How much of your income should you spend on housing?

Whether you're a young professional renting your first flat or experienced homeowner considering a new home purchase, it can be hard to know how much money to spend on housing. In this article, we outline some basic guidelines to help you estimate how much you can afford to pay for your home.

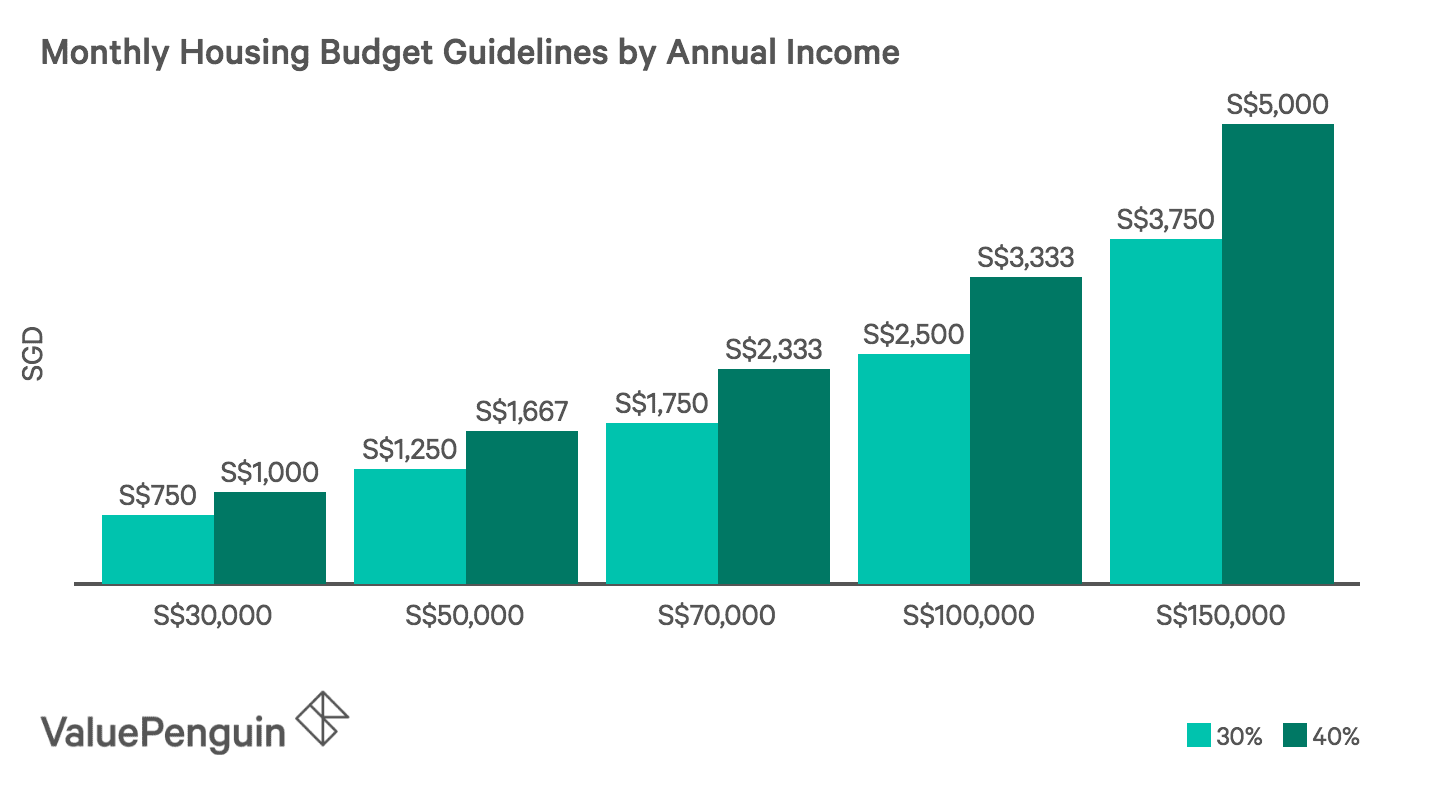

General Rule of Thumb: Housing Costs Should Not Be More Than 30% - 40% of Income

Experts typically suggest that you should spend no more than 30% to 40% of your gross monthly income on housing. These limits are designed to allow room for expenses for basic necessities such as food, transportation, health care and personal savings. It is important to note that these suggested housing budgets include rent and mortgage payments, as well as other related housing costs such as utilities, maintenance or homeowners insurance. For an individual earning S$50,000 annually, this translates to S$1,250 to S$1,667 per month for housing costs.

Tips for Renters: How to Live Within Your Budget

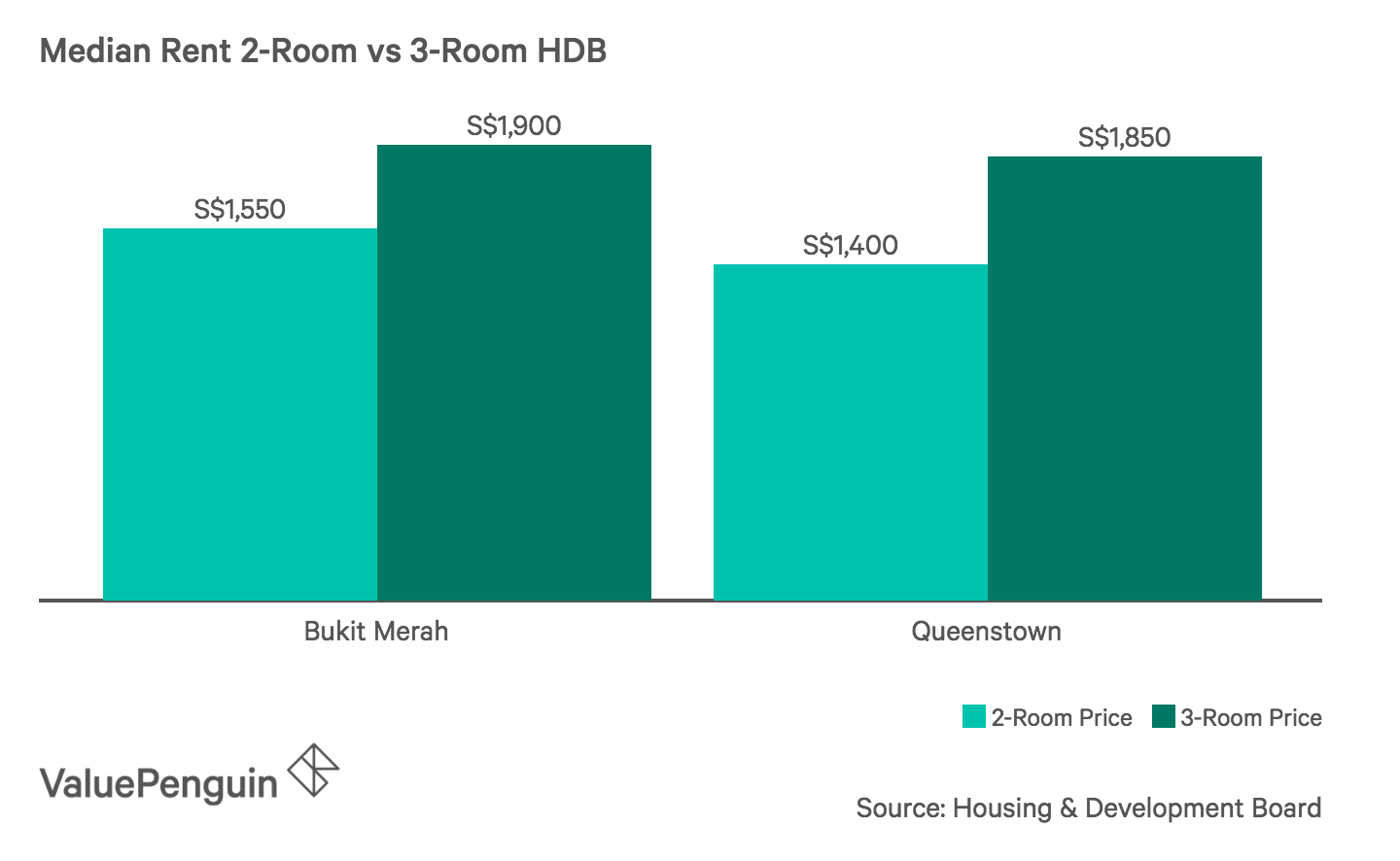

These guidelines may seem very tight to renters that know that rents in Singapore can easily exceed their respective budgets. However, there are many ways to keep your rent costs at manageable levels. First, it may be necessary to live in a less expensive neighborhood. While the median price of a 3-room HDB in Central is S$2,100, renters could consider living further from the city centre where median rents can be as low as S$1,400 for the same sized apartment. Alternatively, you could consider downsizing. For example, median 2-room HBDs in Bukit Merah and Queenstown are 23% and 32% cheaper than the median 3-room HDB in their respective neighborhoods. Additionally, if you feel comfortable sharing an apartment with a friend, moving in with a roommate can cut your housing costs in half.

Tips for Homeowners: Don't Forget About the Total Cost of Homeownership

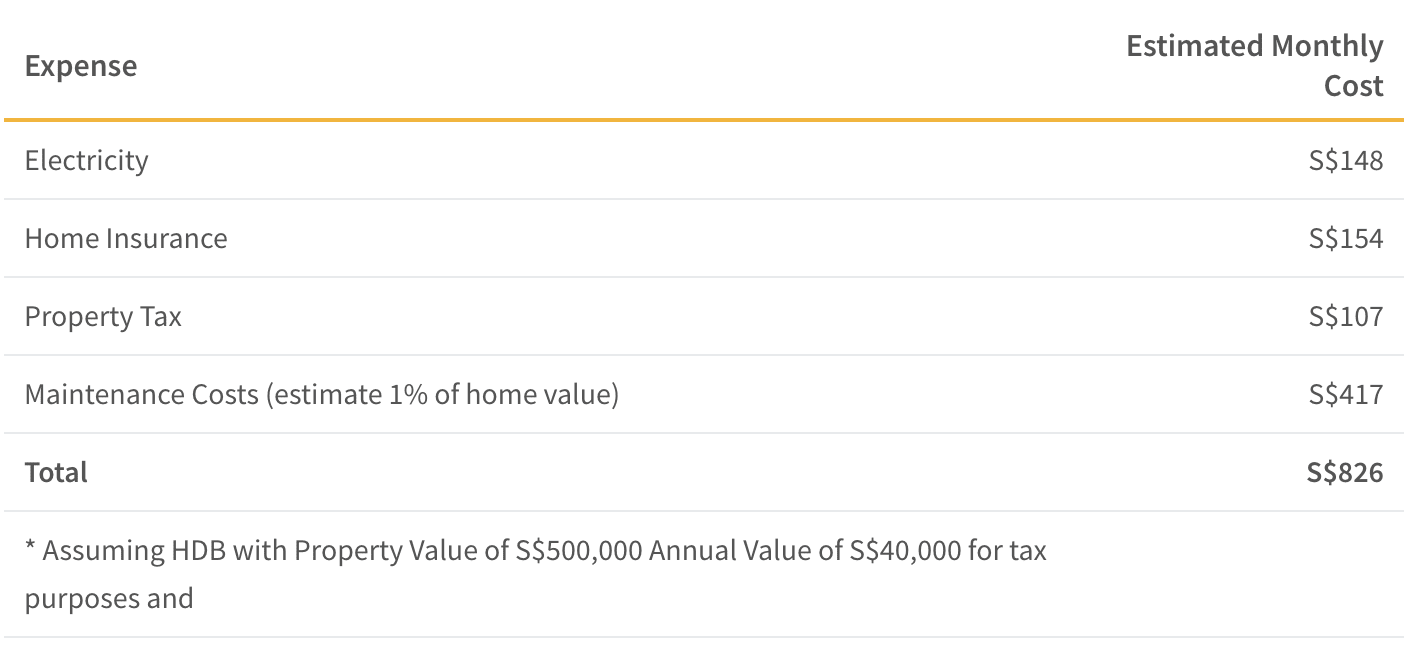

On the other hand, homeowners might find that the guidelines above give them generous room to meet their required home loan payments. For example, monthly payments for a S$300,000 home loan tend to range from S$1,200 to S$1,500, which is much lower than the rent for a similar flat. However, we caution these homeowners to make some additional considerations. First, it is important to have saved up enough money for a down payment, typically about 20%, before purchasing a home. This is worth mentioning because many individuals may earn enough to make mortgage payments, but still not have enough personal savings to make a sizable downpayment. It is also important to consider other costs associated with homeownership. For example, the cost of electricity, home insurance, property tax and home maintenance could easily add up to almost a thousand dollars a month for an average household.

Average Monthly Homeownership Costs

Summary Thoughts: Every Budget is Different

In the end, 30% is simply a number to help give you an idea of how much you can afford to pay for your home. There will always be exceptions to the rule. For example, recent graduates with a significant amount of student debt will need to keep their housing budget low enough to make their loan repayments. On the other hand, high income individuals that are purchasing a second home as an investment might be able to spend more than 30% of their budget on housing. Still, individuals can always use the 30% - 40% maximum as starting point for their housing budgets and adjust accordingly based on their other primary expenses.

This article was first published in ValuePenguin.