10 best savings accounts in Singapore with highest interest rates (December 2024)

PHOTO: Unsplash

Savings accounts have a simple premise, but often come with complex mechanisms for you to earn bonus interest.

When you open a savings account with a bank, you deposit money into it and let that money earn interest. You'll enjoy higher interest rates on a savings account than you would on your normal account (called a checking account).

The issue is that not all savings accounts are made equal. Different banks offer different interest rates, have different minimum sums, and require you to hit different spend/transaction criteria (one of the savings accounts below has 9 types of transactions you can choose from to fulfil!).

So to help you out with navigating savings accounts in Singapore, we've compiled the best savings accounts in Singapore with the highest interest rates in 2024 for different personal and financial needs.

| Savings account | Interest rates (effective interest rates) | Best for |

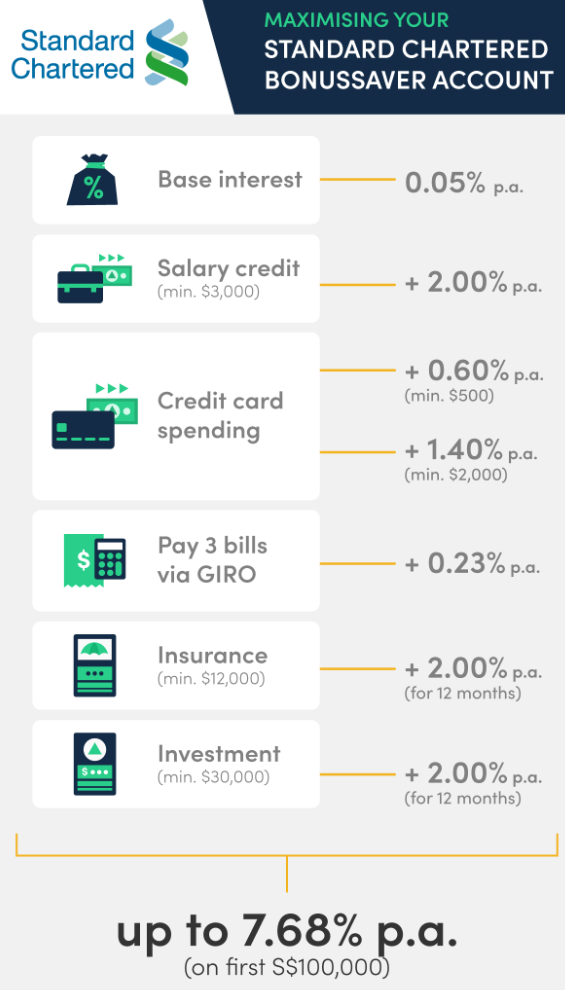

| Standard Chartered BonusSaver | Up to 7.68% (on first $100,000, fulfil 5 criteria) | High spenders |

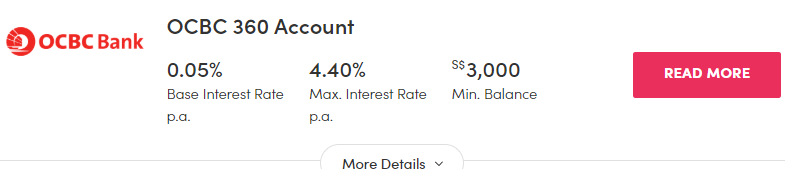

| OCBC 360 | Up to 7.65% (on first $100,000, fulfil 5 criteria) | Lower income earners ($1,800 min. salary) |

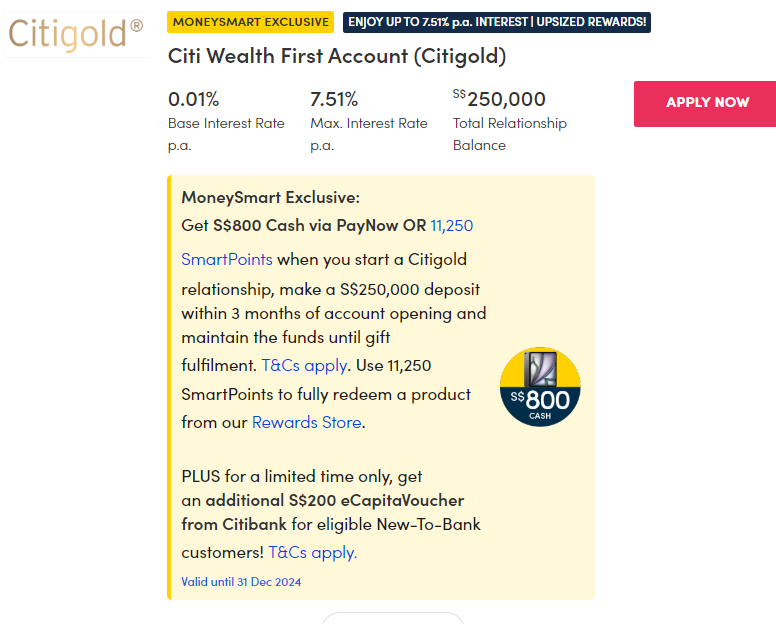

| Citi Wealth First Account | Up to 7.51% (on first $50,000 – $500,000, fulfil 5 criteria) | Those with other Citibank products |

| Bank of China Smart Saver | Up to 7.00% (on first $100,000, fulfil 4 criteria) | High spenders |

| UOB One | Up to 4% (on first $150,000, fulfil 2 criteria) | Freelancers & self-employed |

| Maybank Save Up | Up to 4.30% (on first S$50,000, fulfil 3 criteria) | Home, education, car loan users |

| DBS Multiplier | Up to 4.10% (on first $50,000 – $100,000, fulfil 3 criteria) | Salaried workers |

| CIMB FastSaver | 4.20% (on first $50,000, no criteria to fulfil!) | Young adults starting their careers |

| POSB SAYE (Save As You Earn) | 3.50% (just deposit and maintain money, no criteria to fulfil!) | Students or first-jobbers |

| HSBC Everyday Global Account | Up to 4.25% (register and qualify for the HSBC Everyday+ Rewards Programme) | HSBC Everyday+ Rewards Programme, HSBC Everyday Global Debit Card users |

Most savings accounts require you to jump through a whole bunch of hoops to enjoy their best rates. But let's be realistic here. Most of us aren't going to be taking a home loan, buying insurance from the bank, and investing with the bank-and certainly not all at the same time.

What will you earn if you only fulfil two criteria, such as crediting your salary and spending on your credit card? Here's our realistic summary:

| Savings account and the 2 best requirements you can fulfil | Effective interest rate on first $50,000 | Your earnings on first $50,000 |

| Citi Wealth First Account Save $3,000/month + Spend $250/month |

3.01% (up to first $50,000) | $1,505 per year (~$125 per month) |

| Standard Chartered BonusSaver Credit min. $3,000 salary + Spend $500/month |

2.65% p.a. (up to first $100,000) | $1,325 (~$110 per month) |

| UOB One Credit min. $1,600 salary + Spend $500/month |

3.00% (up to first $75,000) | $1,500 (~$125 per month) |

| OCBC 360 Credit min. $1,800 salary + Save $500/month |

3.20% p.a. (up to first $75,000) | $1,600 per year (~$133 per month) |

| Bank of China SmartSaver Credit min. $2,000 salary + Spend $500/month |

3.40% p.a. (up to first $100,000) | $1,700 per year (~$142 per month) |

| Maybank Save Up Programme Credit min. $2,000 salary + Spend $500/month |

1.25% p.a. (up to first $50,000) | $625 per year (~$52 per month) |

| DBS Multiplier Credit salary + Spend (no minimums) |

1.80% p.a. (up to first $50,000) | $900 per year (~$75 per month) |

| CIMB FastSaver Spend $800/month on CIMB Visa Signature Credit Card (promotion till 30 Sep 2024) |

4.2% p.a. (up to first $50,000) | $2,100 per year (~$175 per month) |

| POSB SAYE (Save As You Earn) No requirements, but cannot withdraw for 2 years |

3.50% p.a. | $1,750 per year (~$146 per month) |

| HSBC Everyday+ Rewards Programme Deposit min. $2,000 and make 5 transactions |

3.25% p.a. interest + 1% cashback (capped at $300 a month) | $1,625 per year (~$135 per month) |

Note: The table above assumes you have a regular banking relationship. If you earn more, spend more, or are a premier or private banking client, you may enjoy better rates. Read the individual sections on each savings account below to find out more.

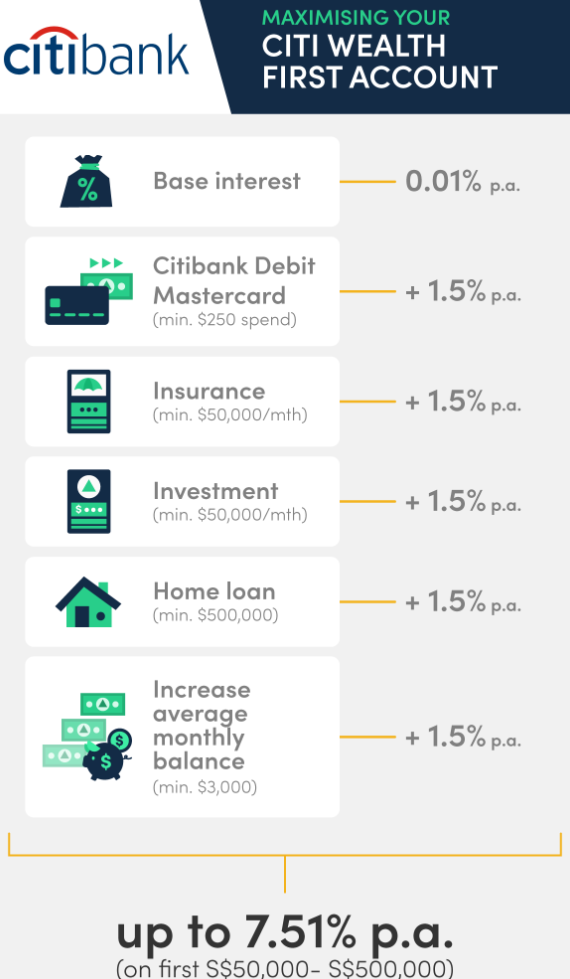

| Citibanking, Citi Priority | Citigold | Citigold Private Client | |

| Deposit amount | First $50,000 | First $250,000 | First $500,000 |

| Base interest rate | 0.01% p.a. | ||

| Spend (min. $250/month on Citibank Debit Mastercard) | 1.5% p.a. | ||

| Invest (min. $50,000/month) | 1.5% p.a. | ||

| Insure (min. $50,000/month) | 1.5% p.a. | ||

| Borrow (min. $500,000 home loan) | 1.5% p.a. | ||

| Save (min. $3,000/month) | 1.5% p.a. | ||

| TOTAL | 7.51% p.a. | ||

The Citi Wealth First Account has a simple mechanic for calculating its total interest rate: base interest (0.01%) + bonus interest (up to 7.50%).

Its base interest starts at 0.01% for everyone, whether you’re a Citibanking, Citi Priority, Citigold, or Citigold Private Client customer. That’s the lowest base interest rate out of all the savings accounts on this list.

Next, beef up that measly 0.01% up with bonus interest rates. You get different bonus rates depending on which of the following categories you fulfil:

If you fulfil all of the transaction categories above, the maximum interest rate you can get with the Citi Wealth First Account is a generous 7.51 per cent.

That's one of the highest rates among the savings accounts this month. Plus, it applies to the first $50,000 to $150,000 in your account, and not just the first $25,000 after the first $100,000 or something like that (looking at you, UOB One). That means 7.51 per cent p.a. is the effective interest rate!

Realistically speaking, most of us can only deposit our salaries in the account, i.e. "Save", and "Spend". If you only fulfil these 2 criteria, you'll earn 3.01 per cent p.a. interest on the Citi Wealth First Account. That's $1,505 earned per year from your first $50,000.

The only advantage to starting a Citigold or Citigold Private Client banking relationship is that the bonus interest rates can apply to a larger sum of money.

For Citibanking and Citi Priority customers, bonus interest rates are applied to only the first $50,000, according to the Citi Wealth First T&Cs (Clause 7). This increases to $250,000 for Citigold and $500,000 for Citigold Private Client.

Citi Wealth First Account

The Standard Chartered BonusSaver savings account used to offer the highest maximum interest rate on a savings account — 7.88 per cent p.a. This maximum rate got reduced to 7.68 per cent p.a. on May 1, 2024, following UOB's rate cut on their flagship savings account.

Here’s a breakdown of the changes that took effect on May 1, 2024:

| Transactions | Interest rates |

| None (base interest) | 0.05% |

| Salary credit (min. $3,000) | +2.00% |

| Credit card spending (min. $500 or $2,000) | + 0.60% OR + 1.40% (min. $2,000) |

| 3x GIRO bill payments (min. $50) | + 0.23% |

| Invest in eligible unit trust (min. $30,000) | + 2.00% for 12 months |

| Buy eligible insurance (min. $12,000) | + 2.00% for 12 months |

| Total interest | 7.68% p.a. |

You'll notice that interest rates for investing or buying insurance with Standard Chartered went up, while the rates for salary credit, credit card spending, and GIRO components fell.

While 7.68 per cent p.a. is high, it isn't easy to hit this maximum interest rate on the Standard Chartered BonusSaver. You'd need to fulfil all five requirements: credit your salary, spend on your credit card, pay three bills, invest, and buy insurance. Tough!

On the plus side, 7.68 per cent p.a. is applied to the entire sum of $100,000, whereas accounts like the UOB One savings account are only going to give the highest interest rate to a smaller sum based on a tiered system. (Check our review of the UOB One account to see the effective interest rates on the entire $100,000 sum.)

Unfortunately, the lowest hanging fruits don't yield high bonus interest. If you fulfil the three easiest categories, salary credit, credit card spending ($500/month), and GIRO bill payments, you only get a rate of 2.88 per cent.

However, the Standard Chartered Bonus Saver savings account does occupy a niche: It gives you pretty high bonus interest just for spending tons of money: if you spend at least $2,000 on your BonusSaver credit or debit card, you get 1.4 per cent bonus interest. Couple that with the salary credit and GIRO bill payments, and you get 3.78 per cent p.a..

Do note that you only get two per cent interest for crediting your salary if you're earning at least $3,000 per month. If you earn less, I suggest the OCBC 360 savings account instead-it'll give you the same 2.00 per cent p.a. interest on your first $75,000 for crediting a minimum salary of $1,800.

Realistically, many of us may only credit our salary and meet the requirement to spend $500 a month. If you only do these two things, you'll enjoy an interest rate of 2.65 per cent p.a. on your first $100,000, inclusive of the base interest rate.

For meeting the same two requirements, the OCBC 360 account (4.05 per cent p.a. on first $100,000) UOB One (3.38 per cent p.a. on first $100,000 or 4.00 per cent p.a. on first $150,000) are going to be a lot more attractive.

Standard Chartered Bonus Saver

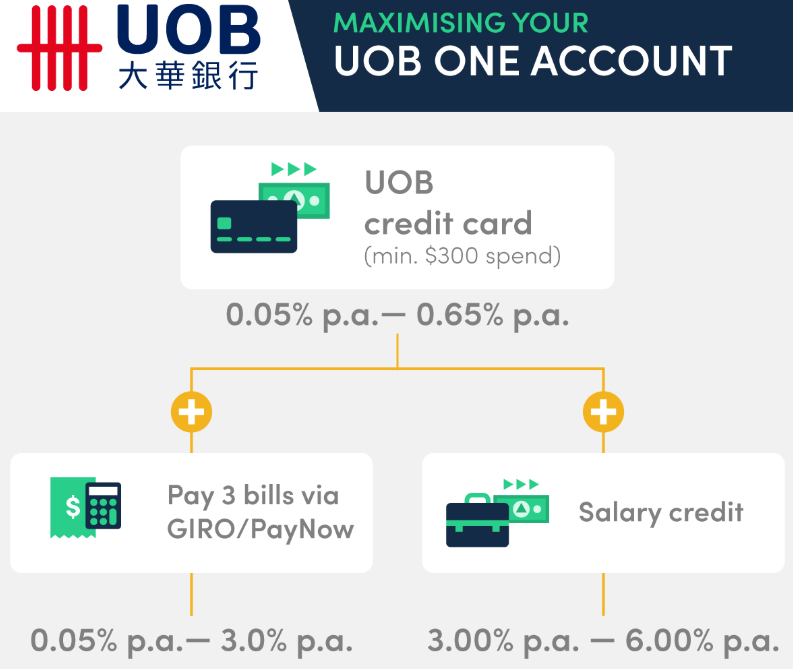

The UOB One Account is kinda famous. It did us all a great service from Dec 2022 to April 2024, offering a rate of up to 7.80 per cent (EIR: 5.00 per cent p.a.) back then for simply spending on a UOB credit card and crediting our salaries to the account.

But Singapore's highest interest savings account relinquished its throne on May 1, 2024, when UOB introduced two new interest tiers and reduced its maximum interest rate to 6.00 per cent p.a. (EIR: 4.00 per cent p.a.). Here are the current rates:

| Account Monthly Average Balance | $500 spend per month on eligible UOB Card | $500 spend per month on eligible UOB Card + 3 GIRO debit transactions | $500 spend per month on eligible UOB Card + credit salary via GIRO (min. salary of S$1,600) |

| First $75,000 | 0.65% | 2.00% | 3.00% |

| Next $50,000 | 0.05% | 3.00% | 4.50% |

| Next $25,000 | 0.05% | 0.05% | 6.00% |

| Above $150,000 | 0.05% | 0.05% | 0.05% |

The UOB One savings account no longer has the highest maximum interest rate for a savings account in Singapore, but it may still be worth it for you. I'm happy to report that at least UOB did not change the mechanics of how to earn bonus interest on the UOB One.

That means the winning quality of the UOB One account remains intact — its criteria to snag the highest interest rate is easy peasy. You only need to fulfil these two requirements:

The eligible cards you can hit the $500 spend on are:

Among these cards, the UOB One Card is one of the best cards to pair with the UOB One savings account.

If you prefer a card with $0 minimum spend, the recently revamped UOB Lady’s Card is right up your alley. And yes, men can apply too!

Don't have a fixed monthly salary? You can still get up to 3.00 per cent p.a. on $50,000 after the first $75,000 with the UOB one account if you pay three bills by GIRO.

This is great for those without a regular pay check, such as freelancers, retirees or homemakers. If you go for this option, the interest rate rises with every additional $30,000 or $15,000 in your UOB One account, up to $75,000.

Everyone is enticed by the six per cent p.a. carrot that UOB dangles, but remember that this is only applied on the $25,000 after your first $125,000 — unlike the Standard Chartered Bonus Saver, which applies 7.68 per cent p.a. on the full $100,000 you bank with them.

What you need to look at is the effective interest rate — the true interest rate on the full amount you deposit in your UOB One Account. Here's how much you'll really earn with different account balances and with the fulfilment of different criteria:

| UOB One Account Effective Interest Rates (EIR) | |||

| Account Balance | $500/month credit card spend | $500/month credit card spend + 3 GIRO debit transactions | $500/month credit card spend + credit salary via GIRO |

| $75,000 | 0.65% | 2.00% | 3.00% |

| $125,000 | 0.41% | 2.40% | 3.60% |

| $150,000 | 0.35% | 2.01% | 4.00% |

| $200,000 | 0.28% | 1.52% | 3.01% |

Simply for crediting your salary and spending $500/month on your credit card, the UOB One Account's four per cent p.a. EIR (on first $150,000) is currently one of the highest out there — second only to OCBC 360's 4.05 per cent p.a..

Comparatively, Standard Chartered will give you 2.65 per cent p.a. to fulfil the same criteria, or 3.45 per cent p.a. if your credit card spending is at least $2,000/month.

UOB One savings account

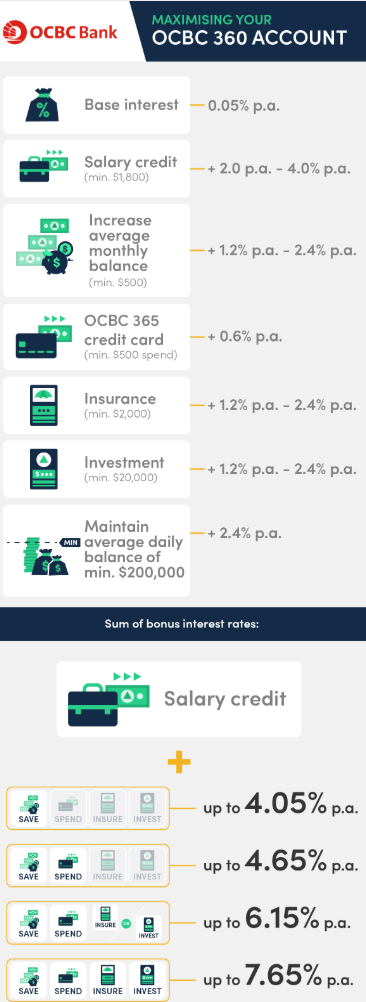

| Transactions | Interest rate (first $75,000) | Interest rate (next $25,000) |

| None (base interest) | 0.05% | 0.05% |

| Salary credit (min. $1,800, GIRO/FAST/PayNow) | + 2.00% | + 4.00% |

| Increase avg. monthly balance (min. $500) | + 1.20% | + 2.40% |

| Spend (min. $500 on selected OCBC credit cards) | + 0.60% | |

| Insure in selected products (min $2,000) | +1.20% | + 2.40% |

| Invest in selected products (min. $20,000) | + 1.20 % | + 2.40% |

| Maintain average daily balance of min. $200,000 |

2.40% |

|

The OCBC 360 savings account is currently one of Singapore's highest interest savings accounts. It starts at a base interest of 0.05 per cent p.a., and gives you varying bonus rates for crediting your salary, spending on your credit card (minimum of $500/month), growing your balance, insuring and investing. If you fulfil several of these requirements, this is what your maximum Effective Interest Rate (EIR) will be on your first $100,000:

To recap, the UOB One account gives you an EIR of up to 4.00 per cent on the first $15o,000 or 3.38 per cent p.a. on the first $100,000.

While that's a lower maximum rate than OCBC 360, don't forget that the UOB One account rewards you with their maximum rates simply for crediting your salary and spending on your credit card.

The OCBC 360 is more complicated than the UOB One, but also more flexible in that there is no one mandatory requirement. This account is perfect for those who don't hit the $3,000 minimum salary requirement many other savings accounts have. You'll get a bonus two per cent just for crediting your salary to the OCBC 360 account through GIRO, FAST, or PayNow. UOB only counts your salary credit if it's via GIRO.

You also get a bonus 1.2 per cent every month that your account balance increases by $500 or more, so that might encourage you to save more even if you don't hit the other criteria.

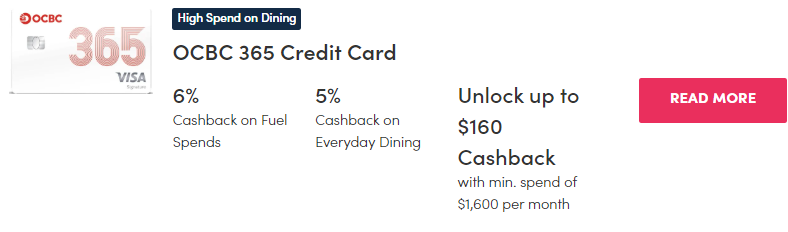

Do note that the $500 monthly spend category for a bonus 0.60% p.a. interest applies only to selected OCBC credit cards:

My top pick is the OCBC 365 Credit Card for its high cashback rates, subject to a minimum monthly spend of $800:

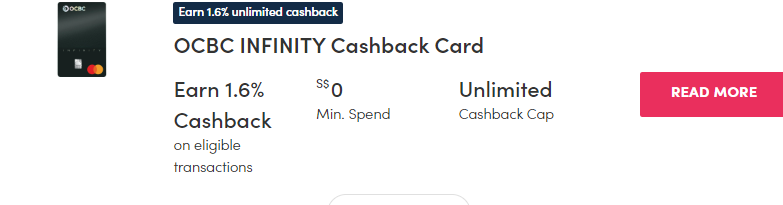

But if you’ve jumped through enough hoops for your savings account and just want a blanket 1.6% cashback rate from your credit card, the OCBC INFINITY Cashback Card is a better fit.

OCBC 360

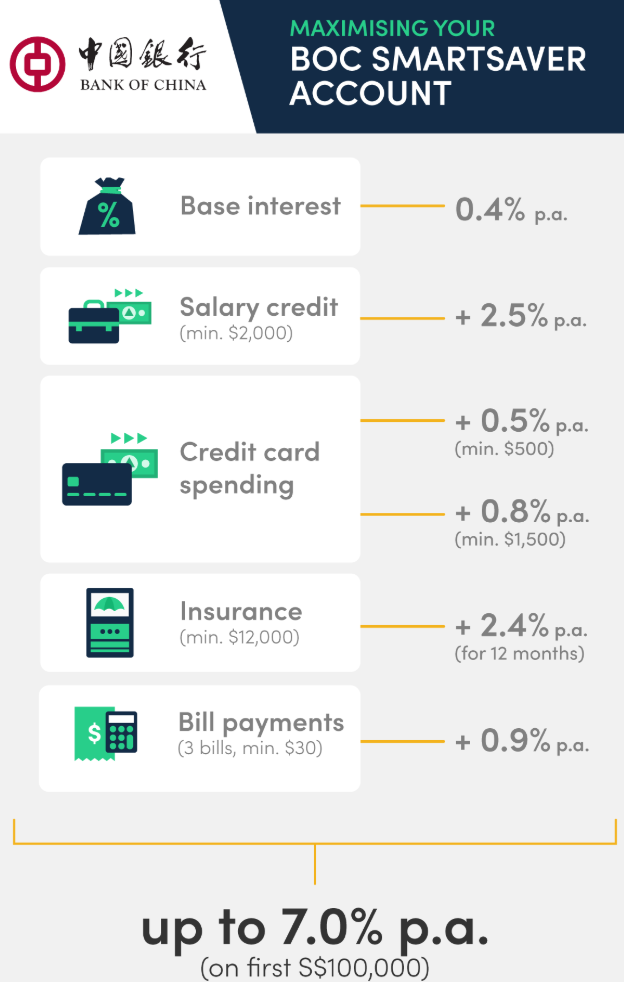

| Transactions | Interest rate |

| None (base interest) | 0.4% |

| Insurance plan spending | + 2.40% p.a. for 12 consecutive months |

| Salary credit | + 2.50% (min. $2,000) |

| Credit card spending | + 0.50% (min. $500) OR 0.80% (min. $1,500) |

| 3x bill payments of at least S$30 each (GIRO or internet/mobile banking) | +0.9% p.a. |

With the Bank of China SmartSaver account, you get a cool 2.5 per cent p.a. just for opening the account and crediting your salary (minimum of $2,500) to it. If raking up a monthly bill of at least $1,500 on your Bank of China credit card is no problem for you, you'll get an additional 0.8 per cent bonus interest.

The Bank of China SmartSaver account also awards a wealth bonus of 2.4 per cent per annum for 12 consecutive months. However, to qualify, you'll have to put down a pretty hefty sum on their insurance products. We're talking a minimum of $12,000 in annual premiums with a 10-year premium term.

If you max out the bonus interest in all categories, you can enjoy a rate of up to 7.0 per cent p.a. on your first $100,000 saved with the Bank of China.

On the other hand, let's say you only credit your salary and spend ($500 a month). Including the prevailing base interest, you'll earn an interest rate of 2.50 per cent + 0.50 per cent + 0.40 per cent = 3.40 per cent on your first $100,000. Still quite decent for low effort on your part!

Bank of China SmartSaver

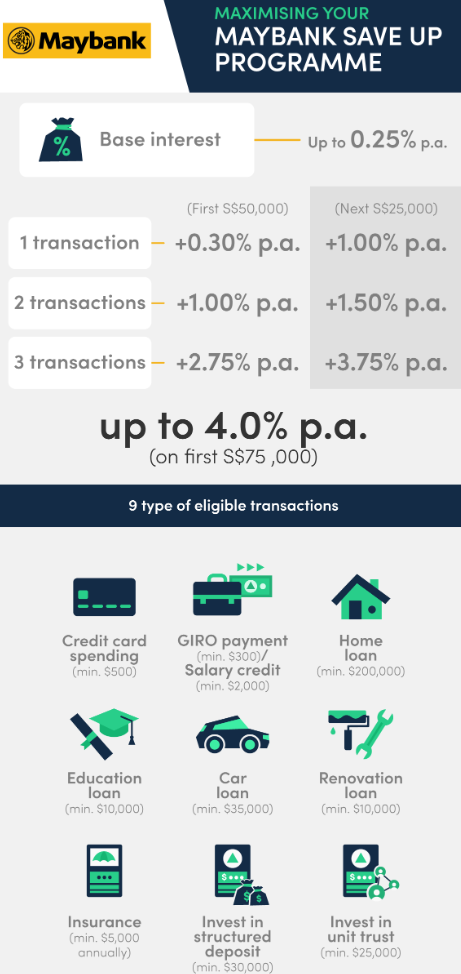

| Interest rates | |||

| Transactions | First S$50,000 | Next S$25,000 | Maximum Effective Interest Rate |

| None (base interest) | Up to 0.25% p.a. | Up to 0.25% p.a. | |

| 1 x transaction | + 0.30% p.a. | + 1.00% p.a. | 0.53% p.a. |

| 2 x transactions | + 1.00% p.a. | + 1.50% p.a. | 1.17% p.a. |

| 3 x transactions | + 2.75% p.a. | + 3.75% p.a. | 3.08% p.a. |

The Maybank Save Up Programme lets you choose from nine different Maybank products/services to get bonus interest:

The Maybank Save Up Programme starts with a higher base interest rate than most other savings accounts. However, the bonus interest rates aren't competitive unless you fulfil three transactions.

Assuming you hit three transactions and start with a bonus interest rate of 0.25 per cent, you'll get 4.3 per cent on your first $50,000 and 5.5 per cent p.a. on the next $25,000.

For comparison, the OCBC 360 account will give you 4.65 per cent p.a. for hitting the three categories of crediting your salary, saving, and spending on your credit card.

Speaking of credit card spending, do note that Maybank only considers credit card spending on the Maybank Platinum Visa Card and Horizon Visa Signature Card. Spending on other Maybank credit cards doesn't count. On the plus side, these cards give you good cash rebates both locally and overseas.

Maybank Save Up Programme

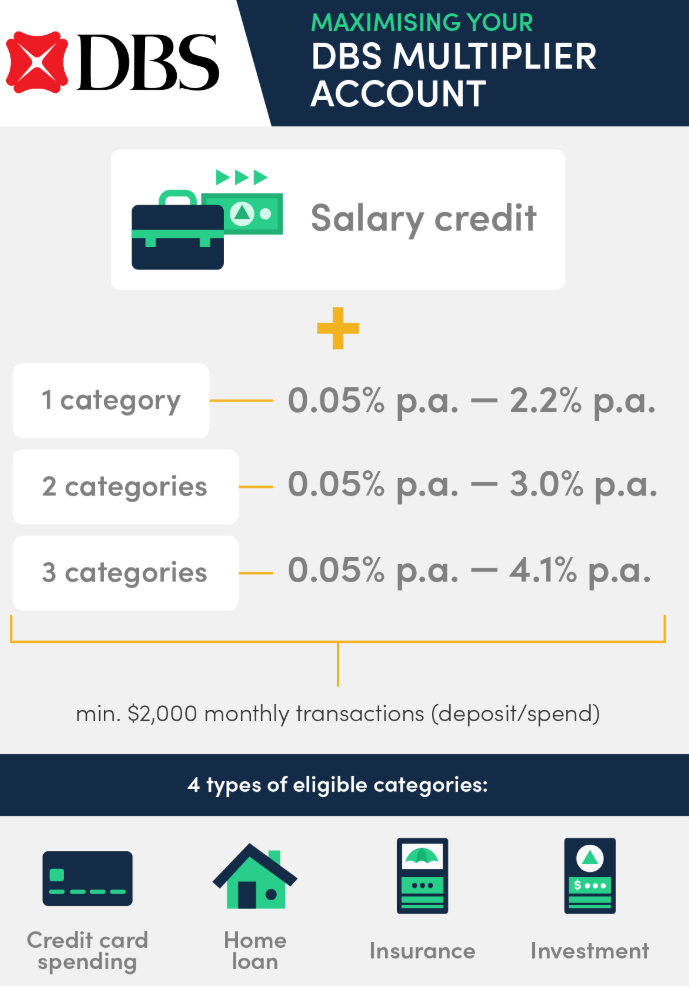

The DBS Multiplier account’s interest rates are only competitive if you hit three categories across credit card spending, home loan, insurance, and investment.

| Total monthly transactions | Income + 1 category | Income + 2 categories | Income + 3 categories |

| First $50,000 | First $100,000 | First $100,000 | |

| $500 to $14,999 | 1.80% | 2.10% | 2.40% |

| $15,000 to $29,999 | 1.90% | 2.20% | 2.50% |

| $30,000 and up | 2.20% | 3.00% | 4.10% |

The rates in the table above apply to you if you credit your salary/dividends/SGFinDex to any DBS or POSB account (yes, it doesn't need to be your DBS Multiplier account!). You need to have at least $500 worth of transactions from one or more of the following categories:

The more categories you hit, the higher bonus interest rates you get.

One thing I really like about the DBS Multiplier is that there is no minimum amount required for the credit card or DBS PayLah! spend. You can also choose either, although I would recommend the credit card route for extra cashback or miles.

You can earn up to 10 miles per dollar with the DBS Altitude Visa Signature Card on your travel spend at Expedia and Kaligo, and 2.2 miles per dollar on other overseas spend.

The DBS Vantage Visa Infinite Card comes with an even bigger welcome miles bonus, although it isn’t the most accessible credit card due to its high minimum income requirement.

What if you don't have any DBS credit card, insurance, or investments? If you're 29 years old or below, you can still earn 1.5 per cent p.a. on the first $50,000. You don't need to credit your salary to a DBS/POSB account, but DBS will still require you to at least use PayLah!.

The good news is that there isn't a minimum amount for PayLah! spend. Just use it to pay for anything, even if it's a $1+ cup of kopi at your local coffeeshop. Easy!

Overall, the DBS Multiplier account makes it easy to earn bonus interest with its zero minimum spend transaction categories and the flexibility to credit your salary into any DBS account, not necessarily the DBS Multiplier.

However, DBS Multiplier account interest rates start pretty low, especially if you don't credit your salary to a DBS/POSB account. Comparatively, CIMB FastSaver's interest rates start at 1.50 per cent p.a. for just opening the account and depositing a minimum of $1,000.

DBS Multiplier

The CIMB FastSaver account is the easiest savings account to earn money with this month. Open your account from now till Dec 31, 2024 and earn up to 5.20% p.a. on your first $25,000 till Feb 28, 2025!

| Account balance | Prevailing interest rate | Bonus interest rate | Total interest rate | Additional interest rate from salary crediting / incoming standing instructions (min. $1,000) |

| First $25,000 | 1.19% p.a. | 2.01% p.a. | 3.20% p.a. | + 0.50% p.a. when you credit your salary or schedule a recurring transfer (Standing Instruction via GIRO) of at least $1,000 + 1.00% / 1.50% (with min $300/$800 monthly eligible spend on your CIMB Visa Signature Credit Card) |

| Next $25,000 | 2.19% p.a. | 1.01% p.a. | 3.20% p.a. | – |

| Next $25,000 | 3.30% p.a. | 0.00% p.a. | 3.30% p.a. | – |

| Above $75,000 | 0.80% p.a. | 2.40% p.a. | 3.20% p.a. | – |

Beyond the first $25,000, you'll still earn up to 3.20 per cent. That's without any conditions to hit a certain credit card spend, requirements to buy insurance, or other hoops to jump through to enjoy this rate.

Admittedly, 3.20 per cent p.a. interest is not a lot. But we have to give the CIMB FastSaver account credit where it's due — it's almost zero effort required.

Their mechanic is as simple as it gets: deposit money, earn interest. The only requirement is to maintain at least $5,000 in your account for you to earn the advertised interest rates. To me, it's almost like a fixed deposit account.

If we assume you hit the requirements to earn 5.2 per cent on your first $25,000, your effective interest rates are:

This account is also perfect for most young adults starting out their career, because of the very low minimum balance of $1,000 (note, however, that you need to maintain $5,000 for the current promotion) and no fall below fee.

CIMB FastSaver

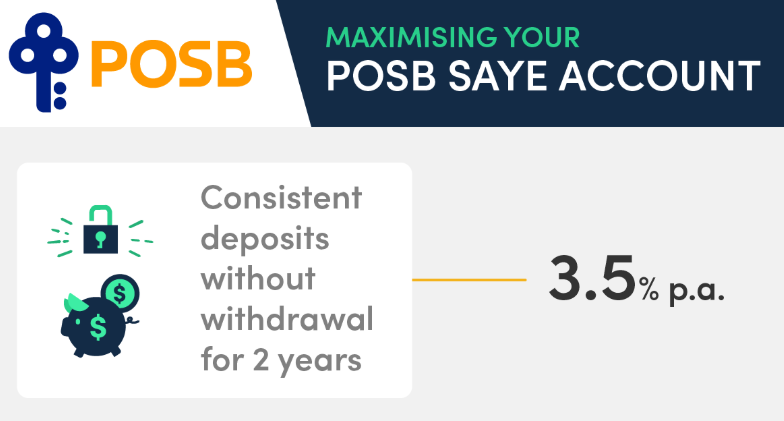

What if you want to open a savings account, but don’t want to do anything but credit money into it? The best zero-effort contender is the POSB SAYE (Save As You Earn) account.

You need to set up a standing order to credit a fixed amount every month (anything from $50 to $3,000) into your SAYE account, then resist the urge to touch it for two years. As a reward for your restraint, you earn 3.5% p.a..

Note that it’s a whole lot less liquid than any other savings account, so for the love of God, please don’t put your emergency stash in here.

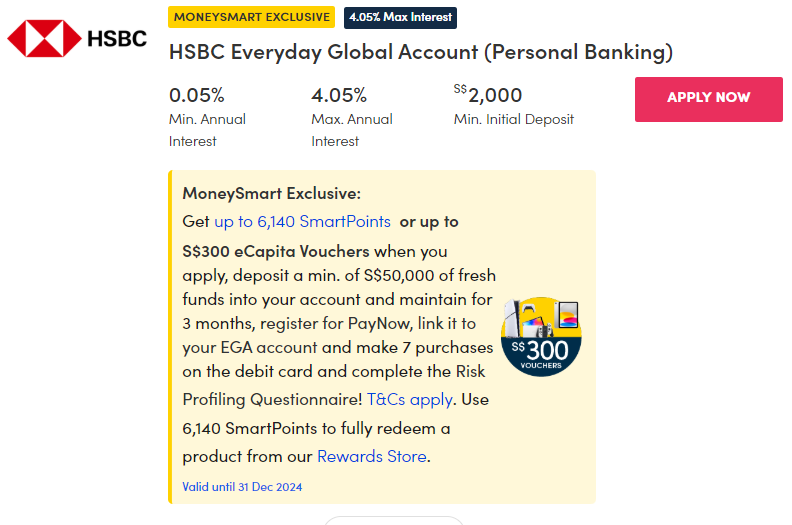

Our last savings account on this list is the most headache-inducing, but also has the highest effective interest rate at the moment due to their ongoing promotion. The HSBC Everyday Global Account is a multi-currency account that also doubles up as a savings account… masquerading as an interest/cashback-earning hybrid. Yikes. Let me explain.

The HSBC Everyday Global Account lets you transact in 11 different currencies, but that’s probably not the reason why you’re reading this article. More importantly for our purposes today, it also functions as a savings account.

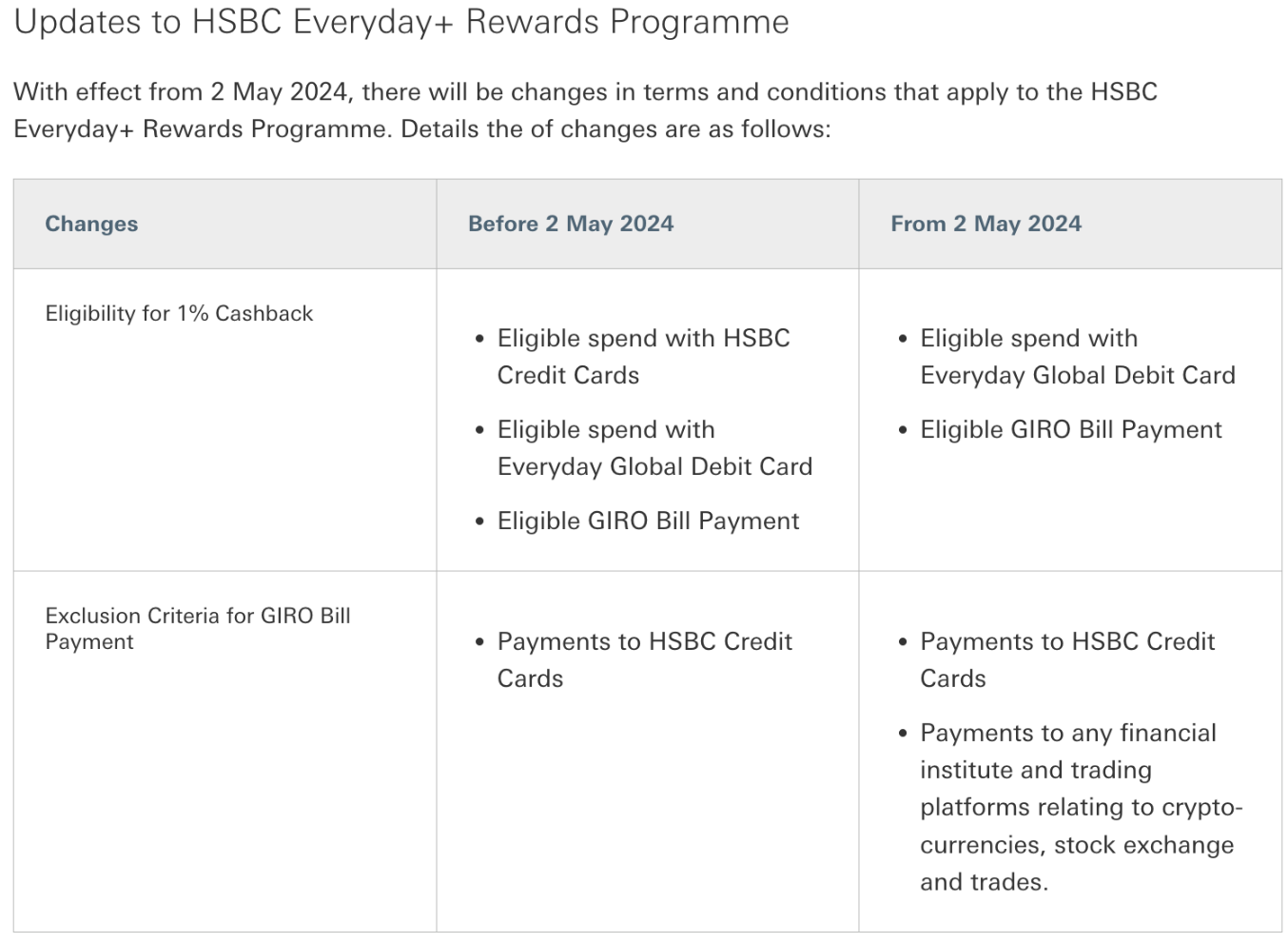

But unlike the others on this list, the HSBC Everyday Global Account doesn’t stack bonus interest the more you spend/save/borrow/invest/insure. Instead, the account works hand in hand with the HSBC Everyday+ Rewards Programme to, overall between the account and the programme, earn you an extra 1% bonus interest and 1% cashback per year.

When you have an HSBC Everyday Global Account and also qualify for the HSBC Everyday+ Rewards Programme, you can earn up to 3.25% p.a. from now to Nov 30, 2024:

On top of that, earn 1.00% p.a. when you qualify for the HSBC Everyday+ Rewards Programme. Combined, that brings your total interest to 4.25% p.a.

The third component above (1% additional interest) comes from qualifying for the HSBC Everyday+ Rewards Programme. Here are the requirements:

Qualifying for the Everyday+ Rewards Programme gets you:

* Note that you can use an HSBC credit card to qualify for the HSBC Everyday+ Rewards Programme, but credit card spending won’t earn you cashback once you qualify the programme. I know, I’m not a fan of this either. This change was implemented by HSBC on 2 May 2024 and is also spelled out in their updated terms and conditions.

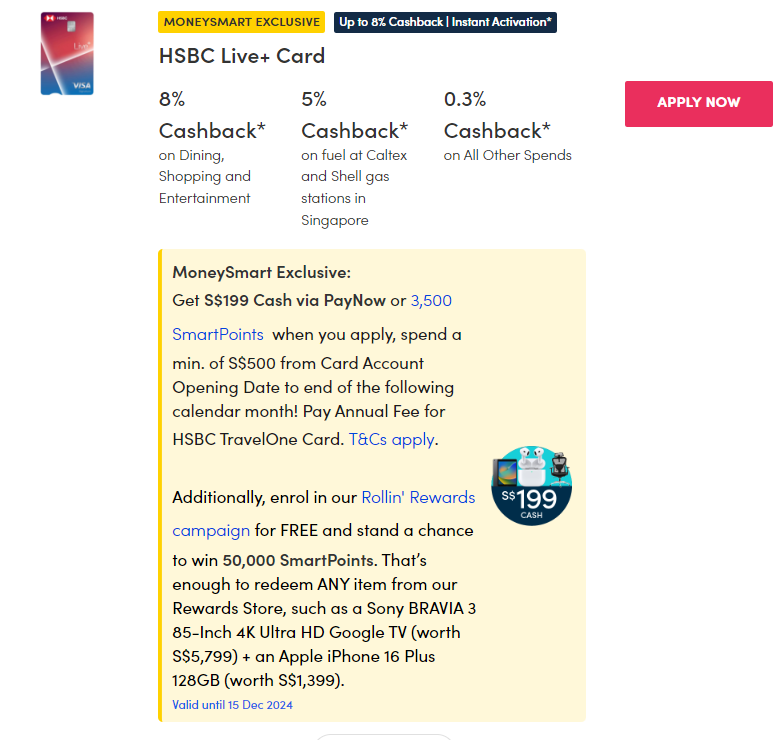

On the plus side, HSBC doesn’t limit you to a select few credit cards for the credit card spending criteria, so take your pick of the HSBC credit cards available. My personal pick is the new HSBC Live+ Credit Card. From now till the end of the year, earn 8% cashback on this card on your dining, shopping, and entertainment spending.

On top of the interest and cashback, HSBC will give you one-time cash bonuses of up to $150 (for Personal banking customers) / $300 (Premier customers) when you deposit at least $100,000 (Personal banking) / $200,000 (Premier Banking) and meets the eligibility criteria above for the first six months.

To register, send an SMS to 74722 with the following format:

EGA<Space>first 9-digit of your Everyday Global Account number (e.g. EGA 123456789)

[[nid:688528]]

This article was first published in MoneySmart.