3 types of bank accounts you should consider opening this new year

PHOTO: The Straits Times file

Getting stuck in mile-long ATM queues is one of the more frustrating moments in a Singaporean’s life—especially when just one metre away, there’s a rival bank’s ATM machine that’s so deserted it seems haunted.

But avoiding ATM machine queues isn’t the only reason you should open more than one bank account. Here are three types of bank accounts you may find relevant to your needs.

There’s a very good reason you should choose to keep your long-term savings separate from the account you withdraw cash from on a daily basis.

If you’ve got a lump sum of cash you hardly touch (such as long-term cash savings or an emergency fund you don’t access unless absolutely necessary), you can enjoy more attractive interest rates by depositing them in a high interest savings account.

Such accounts often reward you with higher interest when you deposit certain amounts of cash and/or when you don’t make withdrawals for a certain amount of time.

Here are a couple of popular savings accounts with the highest interest rates consider:

– CIMB FastSaver Account gives you straight-up 1 per cent interest on any cash in your account up to $10,000 when you’ve got the CIMB Visa Signature credit card.

– On top of the base 0.05 per cent interest rate, the OCBC 360 Deposit Account gives you an extra 2.33 per cent when you credit your salary (minimum $1,800) through GIRO, increase average daily balance by $500, buy (selected) OCBC insurance plans, and buy (selected) investment products from OCBC.

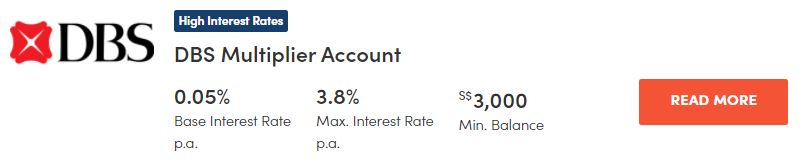

– DBS Multiplier Account comes with a base 0.05 per cent interest rate. You can get up to 2 per cent interest if you do these two things: Credit your salary or dividends or connect your account to SGFinDex and spend at least $2,000 with your credit card, home loan, insurance, or investments via this account.

The DBS Multiplier Account is tiered and you should study this table before you get yourself into it. We know what you’re thinking… money not easy to earn lah.

It’s often a good idea to keep the account you make regular withdrawals from separate from the account you stash your long-term savings in.

Some of the better high interest accounts don’t make withdrawals easy—the banks may not have many ATM facilities, or the account itself may reward you for not making withdrawals (as is the case with the OCBC Bonus+ Account which gives you 0.15per cent a year for no withdrawals, for example).

Your priority when it comes to the account you use for your personal spending should be ease of cash withdrawal and payments. When it comes to availability of ATMs, the clear winners are POSB/DBS, UOB and OCBC.

You also want to check that the account offers internet banking (so you can easily transfer funds to others) and telephone banking if that’s something you need. For Singaporeans who might need to transfer funds to local bank accounts, it makes sense to pick an account from one of the local banks.

Finally, even if you usually pay by credit card, it helps if you can also deduct funds directly from your account using NETS at the check-out counter, for those merchants that don’t accept payment by credit card.

Note that there’s a high chance this account is going to give you a pathetic interest rate. Hence, you should keep just what you need to spend on a monthly basis in there, and then channel the rest of your cash into your long-term savings account. For this reason, pick an account with no or a low minimum balance.

Saving up for something big? It might make sense to open a separate account just for that purpose.

Other than the benefit of keeping the cash separate from your other funds for the avoidance of confusion or making it easier for both you and your partner (if any) to monitor and contribute, you can sometimes also receive perks for stashing your cash in particular accounts.

For starters, all Singaporean parents should have opened a Child Development Account in which their Baby Bonus is deposited in the form of a cash gift and dollar-for-dollar matching of the money they’ve saved for their child’s educational and healthcare expenses.

If you’re looking for something that’s relatively straightforward to just put aside your savings, you could consider accounts like the revamped DBS Multiplier Account, which you can read more about here.

If you credit your salary into a DBS/POSB account, use a DBS/POSB credit card, and the SGFinDex, the Multiplier Account allows you between 0.40 per cent to 3.00 per cent per annum, and unlike fixed deposit accounts, allows you to still have the ability to withdraw your cash in case of an emergency.

Under the Singapore Deposit Insurance Scheme, you receive insurance on your deposits up to $75,000 per bank. That means that if the bank folds and all your money disappears, you’re protected at least for the first $75,000.

If you have $200,000 in savings, it thus makes sense to spread it out over four different banks (note that you will need to keep the cash in different banks, not just different accounts) so you’ll know that every cent’s insured.

This article was first published in MoneySmart.