6 new-launch condos in Singapore: Which is the hot favourite?

PHOTO: Stackedhomes

Every quarter, the local media will publish a story on private home transactions; often one that sensationalises how high or low they are, while completely ignoring the number of new launches. In light of that, I'm expecting another "OMG the private property market is going crazy" report this quarter.

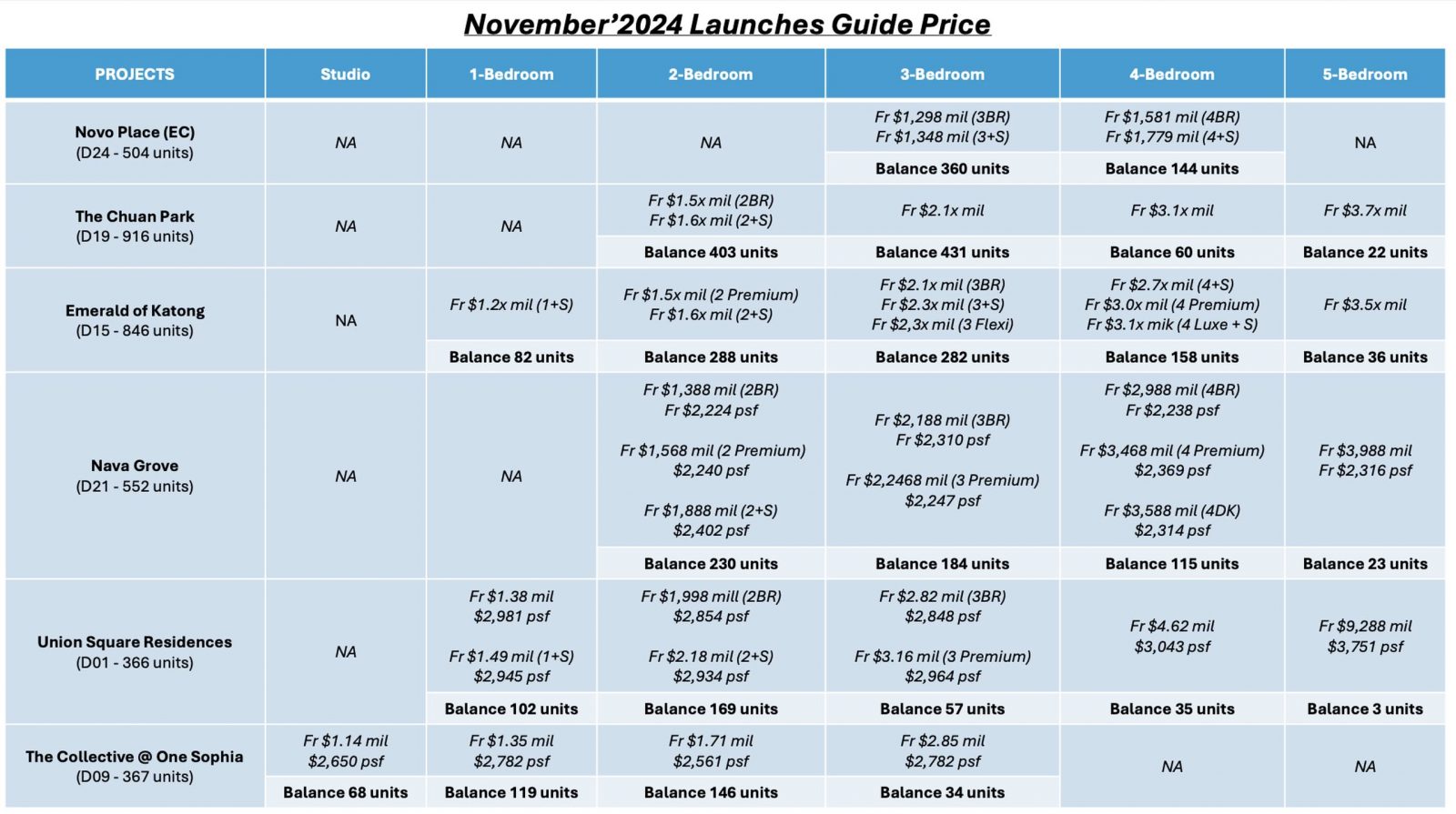

The reason: six new launches this November. Here's a brief rundown, Nava Grove in D21, Union Square Residences in D1, The Collective @ Mount Sophia in D9, Novo Place in D24, and probably 2 of the most anticipated ones, Chuan Park in D19 and Emerald of Katong in D15.

And if you haven't heard, there were reportedly two hour long queues just to get into the show flat at Chuan Park — a combination of its mega development status, a public holiday, and being the first to launch.

Maybe the rush is just to avoid the Chinese New Year period, when the market goes into a bear — like state of hibernation. But the timing is appropriate, because you won't see anything scarier than these prices on Halloween (that is for those who haven't been house shopping for awhile).

For newcomers to the property market in 2024, or those who planned their upgrade five years ago, you might want to sit down for this.

You'll notice that with the exception of the new EC (Novo Place), there's no longer a family-sized three-bedder for less than $2.1 million; the absolute lowest you'll find is the basic three-bedder at Emerald of Katong; and I'd expect those to be snapped up pretty fast.

In any case, it'll be interesting to see the final sales numbers after launch weekend. It's hard to say if launching all 6 at a time is a good strategy (if anything, I highly doubt that if the developers had their way, they would have wanted such a situation), but if we were to look at it positively the buzz it generates could have created more interest for some of the less known new launches.

Given the "lottery" like ballot basis to secure a good unit, it's probably that agents would be telling their buyers to just put down cheques for multiple developments — to see which one would hit.

I also think we'll see a funny situation where the more affluent private buyers move fringeward, while HDB buyers move core-ward

Due to the private home prices, softening rental market, and ABSD hike on foreigners, it's quite likely we'll see private home buyers drift to the fringe. We might see a movement from the CCR out toward the RCR and OCR.

Conversely, the number of million-dollar flats keeps rising. Perhaps some upgraders now see older, prime region flats as a more practical choice than a $2.1 million+ fringe region condo. There's also Prime housing schemes, which could see some lucky BTO buyers moving closer to the city centre.

So I wouldn't be surprised if, in an odd quirk, condo buyers started shifting out to the fringe regions, while HDB buyers moved to retake more city areas or city fringe regions.

It's not a bad thing, and I also hope the new prime housing will increase the allotment of rental housing or 2-room flats, so more lower-income residents can live near the city centre. The city centre is where demand for their work is higher.

The CBD or Orchard, for example, has more need for cleaners, service workers, etc. than a fringe part of Sengkang. Being a prime area, it also means there's a shot at higher earnings (although that probably requires government intervention). It's good for the businesses there, and good for the workers who can live near there.

It's one of the great ironies — not unique to Singapore — that people who most need to live near the city centre are often the ones who can least afford it.

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| MEYER BLUE | $6,285,000 | 1905 | $3,299 | FH |

| KLIMT CAIRNHILL | $5,078,400 | 1432 | $3,547 | FH |

| PINETREE HILL | $3,876,000 | 1464 | $2,648 | 99 yrs (2022) |

| THE RESERVE RESIDENCES | $3,403,100 | 1335 | $2,550 | 99 yrs |

| LENTOR MANSION | $3,244,000 | 1485 | $2,184 | 99 yrs (2023) |

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| KASSIA | $1,013,000 | 474 | $2,139 | FH |

| LENTORIA | $1,313,000 | 538 | $2,440 | 99 yrs (2022) |

| TEMBUSU GRAND | $1,399,000 | 527 | $2,652 | 99 yrs (2022) |

| THE LAKEGARDEN RESIDENCES | $1,411,200 | 592 | $2,384 | 99 yrs (2023) |

| HILLOCK GREEN | $1,534,000 | 624 | $2,457 | 99 yrs (2022) |

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| CUSCADEN RESERVE | $14,100,000 | 3757 | $3,753 | 99 yrs (2018) |

| LEEDON RESIDENCE | $7,500,000 | 2669 | $2,810 | FH |

| REGENCY PARK | $4,825,000 | 2250 | $2,145 | FH |

| ROBIN RESIDENCES | $4,700,000 | 1830 | $2,568 | FH |

| PARC PALAIS | $4,100,000 | 2799 | $1,465 | FH |

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| PARC ROSEWOOD | $660,000 | 431 | $1,533 | 99 yrs (2011) |

| NATURA@HILLVIEW | $700,000 | 441 | $1,586 | FH |

| EUHABITAT | $720,000 | 527 | $1,365 | 99 yrs (2010) |

| TREASURE AT TAMPINES | $784,000 | 463 | $1,694 | 99 yrs (2018) |

| HILLION RESIDENCES | $805,000 | 463 | $1,739 | 99 yrs (2013) |

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| PARC PALAIS | $4,100,000 | 2799 | $1,465 | $2,900,000 | 22 Years |

| LEEDON RESIDENCE | $7,500,000 | 2669 | $2,810 | $2,600,000 | 9 Years |

| THE SHELFORD | $3,080,000 | 1184 | $2,601 | $2,033,634 | 22 Years |

| THE METROPOLITAN CONDOMINIUM | $3,050,000 | 1733 | $1,760 | $1,690,100 | 18 Years |

| HOLLAND MEWS | $2,718,000 | 1270 | $2,140 | $1,668,000 | 20 Years |

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| MARINA BAY RESIDENCES | $2,420,000 | 1055 | $2,294 | -$436,880 | 15 Years |

| SEASUITES | $1,080,000 | 667 | $1,618 | -$65,000 | 12 Years |

| THE ROCHESTER RESIDENCES | $1,350,000 | 872 | $1,548 | -$18,112 | 17 Years |

| ILLUMINAIRE ON DEVONSHIRE | $968,000 | 441 | $2,193 | $12,000 | 14 Years |

| AURA 83 | $808,000 | 484 | $1,668 | $14,200 | 12 Years |

[[nid:708259]]

This article was first published in Stackedhomes.