How does the ABSD affect home purchases by SC/PR or SC/foreigner buyers?

PHOTO: Unsplash

Buying property can be daunting and complicated, especially if it's your first time. On the finances side, it's not just the home loan that you need to take note of. There are also other (often hidden) things to take into account, such as the stamp duty and property tax.

For Singaporeans, if it's their first home, they're exempted from paying the Additional Buyer's Stamp Duty (ABSD).

But it's a different story for those buying with a PR or foreigner. Even if it's their first residential property, they're still subjected to the ABSD.

The Additional Buyer's Stamp Duty (ABSD) is a stamp duty paid on top of the Buyer's Stamp Duty (BSD). The payable rate depends on the residential status of the buyer and the number of residential properties under their name. How much you'll need to pay is then computed based on either the property price or valuation, whichever is higher.

It's a form of cooling measure designed to bring down property prices and make housing more affordable for Singaporeans. So the ABSD rates are higher for non-Singaporeans and those with more than one residential property.

The latest change in the rates took effect on April 27, 2023, almost 1.5 years after the previous hike in December 2021. The ABSD rate for Singaporeans was increased from 17 per cent to 20 per cent for their second residential property.

| ABSD rate from 16 Dec 2021 to 26 Apr 2023 | ABSD rate from 27 Apr 2023 | Increased by | ||

| Singapore citizens | First residential property | 0% | 0% | – |

| Second residential property | 17% | 20% | 3% | |

| Third and subsequent residential property | 25% | 30% | 5% | |

| Permanent Residents (PR) | First residential property | 5% | 5% | – |

| Second residential property | 25% | 30% | 5% | |

| Third and subsequent residential property | 30% | 35% | 5% | |

| Foreigners^ | Any residential property | 30% | 60% | 30% |

| Entities | Any residential property | 35% | 65% | 30% |

| Trustees | Any residential property | 35%* | 65% | 30% |

| Housing developers | Any residential property | 35% (remittable) + 5% (non-remittable) | 35% (remittable) + 5% (non-remittable) | – |

*The ABSD rate for trustees was from 9 May 2022 to 26 April 2023.

Excluding Nationals and Permanent Residents of Iceland, Liechtenstein, Norway and Switzerland, and Nationals of the United States of America, who will be subject to the same stamp duty rate as Singaporeans.

For PRs buying their second residential property, the increase was even higher from 25 per cent to 30 per cent. It's even steeper for foreigners, as the ABSD rate has been doubled from 30 per cent to 60 per cent.

The thing about the ABSD is that if you're buying with another person with a different profile (that is, based on the number of residential properties owned and residency status), the ABSD payable will be based on the profile with the higher ABSD rate.

The exception to this is for buyers who are:

Under the respective Free Trade Agreements (FTAs), they will enjoy the same stamp duty rate as Singaporeans. They can apply for the remission via the e-Stamping Portal.

Here's a breakdown on how the ABSD can affect your home purchase.

For PRs, whether or not they're buying their first residential property on their own or jointly with a Singapore Citizen (SC), they'll need to pay five per cent ABSD.

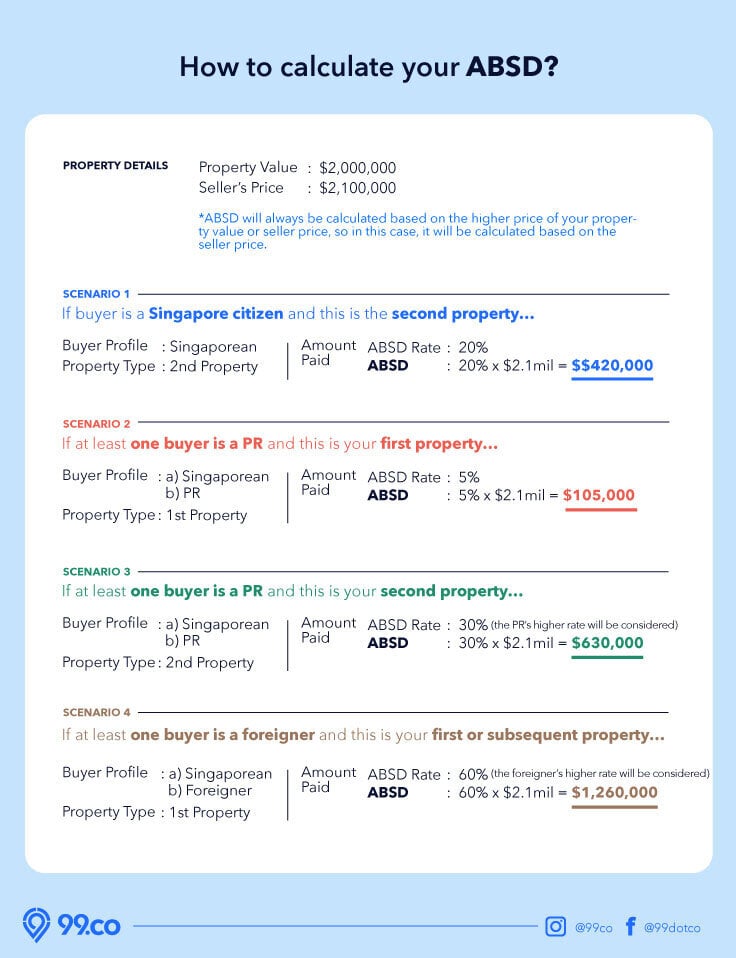

So if you're a Singaporean planning to buy a house with a PR, and this is the first residential property for both of you, you'll need to pay the five per cent ABSD.

Let's say you're buying a $2.1 million condo. The ABSD to be paid will be 5 per cent ⨉ $2.1 million = $105,000.

In the case where the SC already has a house, the joint purchase with the PR will be considered to be the SC's second home purchase.

This means that the SC's ABSD rate will be 20 per cent, while the PR's ABSD rate is five per cent.

The ABSD payable will be the higher rate, which is the SC's rate at 20 per cent. This translates to an ABSD of $420,000 for a $2.1 million condo.

On the contrary, if it's the PR that already has a house, the joint purchase will be the PR's second home purchase. So they're subject to the 30 per cent rate.

For a $2.1 million condo, the SC-PR buyer will have to pay an ABSD of S$630,000.

Let's say both you and another person (a PR) have a residential property on your own, and plan to buy another house together.

As of 27 April 2023, the ABSD for SCs buying a second home is 20 per cent. For PRs buying a second home, it's 30 per cent.

In this case, the payable rate will follow the PR's rate, which is 30 per cent.

So for a $2.1 million condo, the ABSD rate payable is 30 per cent ⨉ $2.1 million = S$630,000.

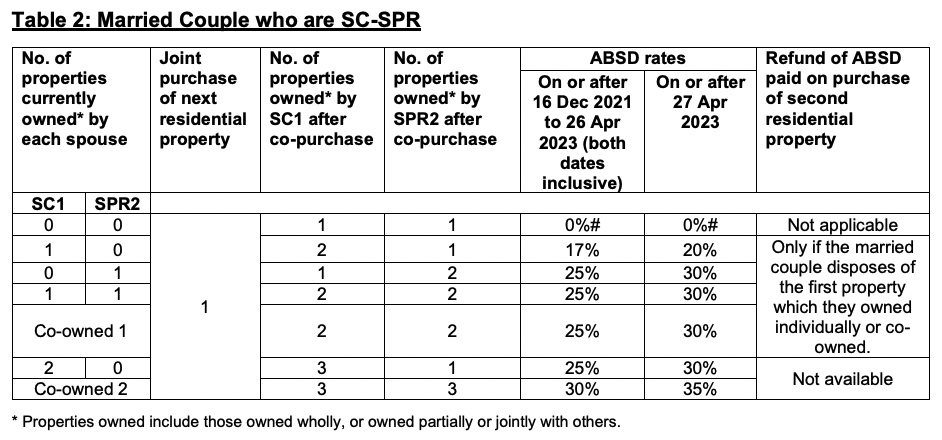

This table from IRAS summarises the ABSD rate to follow for SC/PR buyers, based on the number of residential properties owned and residency status.

Regardless of whether it's the first home purchase or not, foreigners have to pay a 60 per cent ABSD, as of April 27, 2023. This is an increase from 30 per cent.

On top of that, since the highest ABSD rate for SCs is 30 per cent (for the third and subsequent home purchase), the ABSD rate payable for a joint purchase with a foreigner will follow the foreigner's rate of 60 per cent.

This means for a $2.1 million condo, the ABSD payable is 60 per cent ⨉ S$2.1 million = S$1,260,000.

This table summarises the ABSD rate to follow for SC/foreigner buyers, based on the number of residential properties owned and residency status.

The good news is that if you're buying as a married couple, you may be eligible for the ABSD remission.

With the ABSD remission, you don't have to pay the ABSD. But you'll need to meet certain criteria. The main thing is that the house has to be:

Let's say you're a Singaporean and your spouse is a non-Singaporean (either a PR or foreigner). If both you and your spouse don't have any other residential properties, you can apply for the ABSD remission. So you don't have to pay the ABSD.

You can apply for the ABSD remission via the e-Stamping Portal.

But the main thing is that the house must be jointly bought by both of you.

If you and your non-Singaporean spouse are buying a second house together to upgrade (for instance, from an HDB flat to a condo), you'll be subjected to a higher ABSD rate.

This will be 30 per cent on the second house if your spouse is a PR, or 60 per cent if they're a foreigner.

You'll have to pay the ABSD first, even if you plan on selling the first home.

If you manage to sell it within six months from

you may be eligible for the ABSD remission to get a refund.

Likewise, to be eligible for the remission, the second residential property must be purchased under both names.

You can apply for the remission through the e-Stamping portal. For more information on the refund application for the ABSD remission, you can also refer to IRAS' guide.

Take note that this ABSD remission doesn't apply if you're upgrading from an HDB flat to another HDB flat, eg. from a four-room to a five-room flat. Or if you're upgrading to a new EC bought from the developer.

After all, for public housing and ECs bought from developers, you'll have to dispose of your old flat within six months of the sale completion of the flat (i.e. getting the keys to the flat).

The ABSD remission is only for buying the first property, or the second property if you sell the existing property.

So if you're buying a third property together, you'll have to pay the ABSD and won't be able to get a refund.

For an SC/PR couple, the ABSD rate will be 35 per cent. On the other hand, SC/foreigner couples will be subject to the 60 per cent ABSD rate.

[[nid:626658]]

Even if you're engaged, you won't be eligible for the ABSD remission.

The ABSD has to be paid within 14 days of signing the Option to Purchase (or Sale and Purchase Agreement if no OTP is issued). So if you want to qualify for the ABSD remission, you'll have to register your marriage beforehand.

This also means that if you're planning to buy a house with your parents or siblings, you won't be able to qualify for the remission.

This is one of the first things we mentioned about the ABSD remission earlier, but we thought we should highlight it here again.

The ABSD remission is only applicable for those with at least one Singaporean spouse. So it's not applicable for PR-foreigner couples.

And given that the ABSD rate to pay will be based on the profile with the higher rate, regardless if this is the first residential property together or the third one together, the ABSD payable will be 60 per cent.

ALSO READ: How being a 'super-aged' country by 2026 will impact the housing market