Premiums? Sum assured? Here are the terms you need to know about life insurance in Singapore

PHOTO: Unsplash

Insurance terms can be confusing for some of us, especially when we first start buying insurance.

Despite many insurance agents and financial advisors throwing in the benefits of what their company’s product can bring, you will still be at the losing end if you are not aware of what the typical jargons are in insurance.

So today, we are here to let you know what you need to know about life insurance. This will be a two-part article, with the second part providing further details on the type of premiums and life insurance plans.

There are a few parties you have to note when you are purchasing a life insurance policy.

Even though most of us would buy life insurance for ourselves, resulting in an overlap of the terms, we would have occasions where we would purchase life insurance for our loved ones instead.

First, we have to define what a life insured is. A life insured is someone that the policy covers in the event of an event (e.g. death) specified in the policy.

An applicant is someone who applies for the policy and is usually the policy owner, which is someone who owns the policy. And the beneficiaries are those who will receive the policy’s benefits.

There is no single type of life insurance plan, each serving different purposes. You can classify the different life insurance into three categories, with some sub-categories overlapping. The three categories are Participating, Non-Participating, and Investment-Linked Policies (ILPs).

Participating policies are life insurance policies that provide a bonus (be it yearly or at the end of the policy term) along with the sum assured.

These bonuses are non-guaranteed, which means that the extra bonuses stated in the policy are more of a guideline than an obligatory cause (the only guaranteed sum in your life insurance policy is the sum assured). These bonuses can be paid in terms of annual bonuses, terminal bonuses at the end of the insurance term, cash dividends, and interim bonuses.

Non-participating policies do not provide a non-guaranteed bonus as they do not enjoy the benefits of investment in the participating fund of the life insurance company.

Term life insurance tends to fall into this category; some life insurance companies will have a separate insurance pool for non-participating policies, which might not have any investments into assets that can grow the pool and provide bonuses.

Investment-Linked Policies (ILP) are policies in which cash values are entirely non-guaranteed as all of the premiums paid will be invested in an underlying fund. The life insured bears 100 per cent of the investment risk.

Now that you know about the parties involved, as well as the type of life insurance plans, we would want to know what are the terms for paying for the life policy, as well as what kinds of benefits do we receive when the policy has been terminated due to death, policy term expiry, or intentional early termination.

A premium is an amount you pay either yearly or monthly (in some cases, bi-yearly or quarterly) to the insurance company to contribute to your policy.

The total premiums paid, or premiums paid to date, are the premiums paid from the beginning of the policy until the current state of the life insurance (or when talking about death benefits, the day of the unfaithful event of passing on).

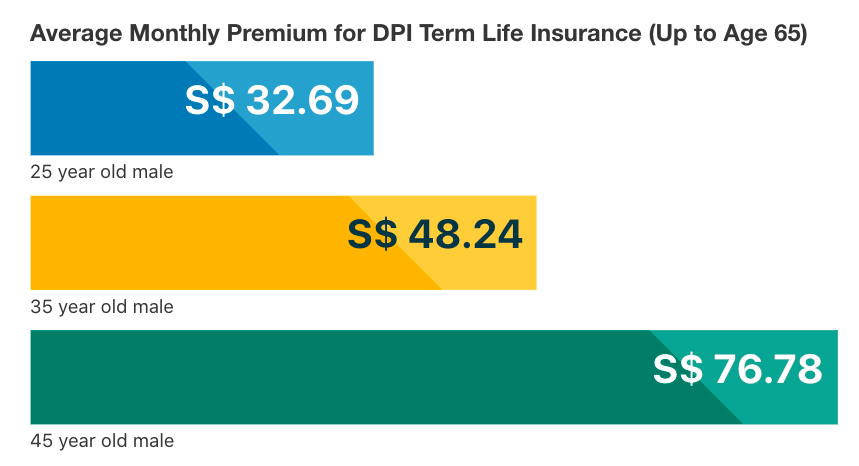

Here are the average insurance premiums paid by a typical person in Singapore throughout different stages of his life. Do note that premiums tend to differ for age, gender, and lifestyle choices (if you smoke).

The cash value, also known as the policy value, is how much your policy is worth at the moment or how much money your policy holds. Term-Life Insurance and Universal Life Insurance do not have cash value.

For non-participating policies, your cash value is usually determined by the total premiums paid. In contrast, for participating policies, your cash value will include your bonuses and dividends made from the investment assets of the participating pool fund.

[[nid:575870]]

As for ILPs, your cash value is the valuation of your asset performance.

Based on your cash value, your insurer would provide certain benefits depending on the plan you have selected. Such benefits include taking loans against the policy's cash value or even making partial withdrawals.

Insurers will not provide those benefits during the start of your life insurance policy as there is no sufficient cash value in the policy to keep it running.

Having a policy with cash value also allows you to activate Non-Forfeiture Options, such as surrendering your plan and getting back surrender value or using it to purchase Paid-Up or Extended-Term Insurance plans.

Every Insurance Policy has a termination date. For Whole-Life Insurance, the termination date is 99 years, whereas, for endowment plans, it depends on how long the insurer chooses to set the plans for ten years, 15 years, 20 years etc. At the end of the maturity period, insurers would estimate the total cash value of the policy.

You would receive maturity benefits when your policy terminates in terms of the sum assured, plus terminal bonuses.

Your surrender value is the value you will receive if you surrender/fully withdraw from/terminate your policy early.

This is where most people get confused between cash value and surrender value. In fact, the surrender value is often lower than your cash value.

[[nid:581085]]

Despite what insurers claim, you can surrender your policy at any time, but they will penalise you when you fully surrender your policy. This is to keep you within the policy for as long as possible and prevent shady short-term transactions.

In Singapore, the MAS and LIA have provided a disclosure guideline for insurance companies in Singapore to follow if they want to operate.

Such guidelines include the information provided in the Benefit Illustration. A particular section called the “Effects of Deductions To-date” provides a table that tells you the difference between “value of premiums paid to date” and “total surrender value”.

These effects of deductions to date are the penalty that insurers charge for early termination, which is used to cover the marketing and administrative cost of the company.

Now, the sum assured is the most straightforward term in life insurance, yet, the most misunderstood. The sum assured is the amount of money predetermined by your insurer that is provided to your beneficiary if an insured event occurs.

An Insured event can include accidental death and dismemberment for personal accident plans and riders, critical illness for critical illness plans and riders, or death or Total Permanent Disability (TPD) for base life insurance plans.

Note that the sum assured is the minimum guaranteed amount that the insurer is obligated to pay as stated in the policy contract. If the sum assured of your life insurance plan is $100,000 for death, the insurance company has to pay you a $100,000 minimum, which brings me to my next point.

Life insurance covers your beneficiaries after death, so the death benefit is what your beneficiaries would receive in the event of your death.

Now, because some people tend to buy riders, which add on along with the sum assured, such as accidental death benefit, which provides additional coverage with the sum assured in case of a death caused by accident, other people would also get participating insurance, such as endowments, that provides non-guaranteed bonuses and the assured sum as the death benefit.

For Investment-Linked Policies, the death benefits would be the policy's cash value, with some insurers providing a small extra percentage.

In summary, death benefits differ in types of life insurance plans:

For Non-Participating Life Insurance Policy Plans, Death Benefit = Sum assured + Riders (if included).

For Participating Life Insurance Policy Plans (Whole Life; Endowments; Annuities), Death Benefit = Sum Assured (Guaranteed) + Annual Bonus (Non-Guaranteed) + Riders (if included).

Typically, for ILPs, Death Benefit = Cash Value * (100 per cent +n per cent) + Riders (if included), where n is the percentage promised by some insurers for that specific plan.

Now that you understand more about the different terminologies for insurance, you can be more confident in understanding your policies better.

This article was first published in ValueChampion.