We make $300k per year and own an EC. Should we sell and buy 2 condos?

PHOTO: Stackedhomes

Greetings to the Stackedhomes team!

We have been following your great analysis posts and beautifully curated videos, which have been very helpful to the aspiring property upgraders and home seekers. Kudos and please keep up the great work!

As we are planning on our asset enhancement journey, we would like to seek some expert views on our situation and next best strategy. Preferred objective for investment property is to collect some rental income while awaiting for capital appreciation in a three-five year time horizon.

Below, we lay down our background information and current options for your analysis and advice please.

Background

We are a married couple in our early 40s, currently with no kids. We jointly own a private property that is valued at around $1.3 million (there's outstanding loan of about $600,000) in the sengkang vicinity and is collecting some rental income (around $2,000). Current property is within one kilometre of a popular primary school and close proximity to amenities and shopping mall, hence, value should be able to hold.

For the next homestay property, we have done some preliminary research and found the Potong Pasir/Woodleigh area to be quite attractive. This is because we considered that:

For the next investment property, we are open to different locations though the primary objective is the ability to collect rental income and capital appreciation with a three-five year horizon.

Current planning options:

Current financial situation

Male: Earning about $150,000 per annum. Cash plus CPF is about $700,000.

Female: Earning about $150,000 per annum. Cash plus CPF is about $500,000.

Given the above information, we would like to seek some advice on our planning options and perhaps, some recommendations on potential projects that would work in our case.

Further clarifications

We are currently staying at Treasure Crest (TC) which is going to MOP in Sept 2023. Points (2) and (3) are both selling one and buying two, one for own stay and one for rent.

Main difference is the sequence of the procedure. For (2) is to decouple, buy own stay property, sell TC and buy unit for rent. For (3) is to sell TC and buy own stay and unit for rent. Option (2) will incur cost for decoupling but gives us time and greater flexibility to explore and pick units without having to rush into making a decision. Option (3) will save some cost but it would imply we have to at least ensure we have a place to stay after selling TC.

Hope my clarification is good enough.

Cheers

Hi there,

Thank you for your kind words and support for our content!

While we don't know the nature of your jobs (it seems to be a very comfortable current financial situation since you don't have kids or a car), we would just like to mention that it's really important given the high-interest rate climate now to be very realistic on how stable your jobs will be.

This is because while selling one and buying two condos can work out well financially, it can also be a big risk if not done correctly, or if either of you faces the risk of losing your job.

So even though you probably already know this, it's still important for us to highlight this for others out there who may be in the same situation.

In this article we will run through:

| Description | Amount |

| Maximum loan based on assumed age of 42 and fixed annual income of $150K | $1,239,296 (23-year tenure) |

| CPF + Cash (not including proceeds from the current property) | $700,000 |

| Total loan + CPF + Cash | $1,939,296 |

| BSD based on $1,939,296 | $66,564 |

| Estimated affordability | $1,872,732 |

| Description | Amount |

| Maximum loan based on assumed age of 42 and fixed annual income of $150K | $1,239,296 (23-year tenure) |

| CPF + Cash (not including proceeds from the current property) | $500,000 |

| Total loan + CPF + Cash | $1,739,296 |

| BSD based on $1,739,296 | $56,564 |

| Estimated affordability | $1,682,732 |

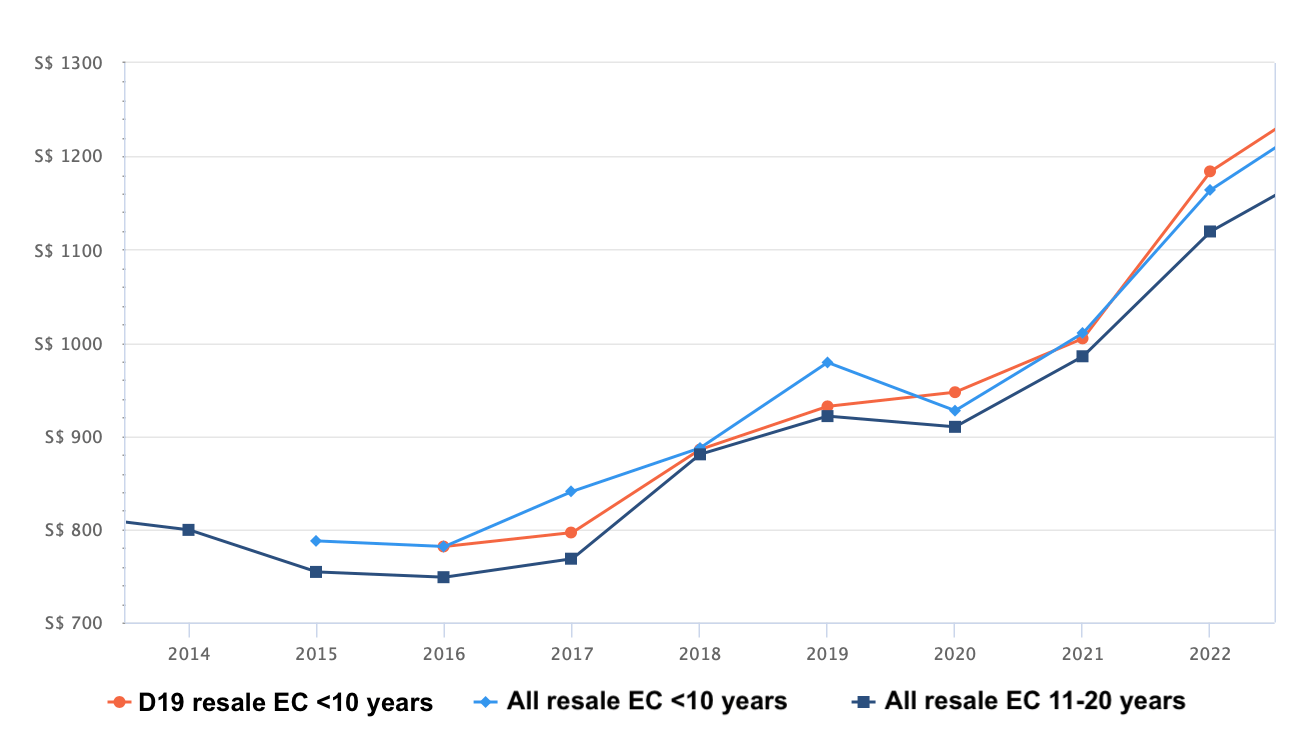

Executive Condominiums (ECs) often experience an appreciation in value after fulfilling their Minimum Occupation Period (MOP), though there may be exceptions.

This trend can be attributed to the eligibility criteria and income ceilings in place when purchasing an EC from a developer. Once the MOP is fulfilled, there are no longer any eligibility or income restrictions (aside from limitations on selling to foreigners until the 10th year), which can broaden the potential buyer pool for resale ECs.

Let's take a look at the performance of ECs at different ages.

As there are no resale transactions for ECs under 10 years old in District 19 in 2014 and 2015, we can only use data from 2016 - 2022.

However, a look at the chart reveals why it's not possible to extrapolate EC growth from this period of time. 2016 was a market low and 2022 was a market high. Annualised returns here would not be representative of long-term growth as it's just one part of the property market cycle — growth. Generally, it's best to pick two points in the cycle which are similar to get an average growth rate between one cycle to another.

Because of this, we will look at data for all ECs over a longer period for a fairer representation.

| Year | Avg PSF of all resale ECs (regardless of age) | YoY |

| 2000 | $430 | – |

| 2001 | $413 | -3.95 per cent |

| 2002 | $346 | -16.22 per cent |

| 2003 | $364 | 5.20 per cent |

| 2004 | $357 | -1.92 per cent |

| 2005 | $343 | -3.92 per cent |

| 2006 | $328 | -4.37 per cent |

| 2007 | $405 | 23.48 per cent |

| 2008 | $473 | 16.79 per cent |

| 2009 | $492 | 4.02 per cent |

| 2010 | $600 | 21.95 per cent |

| 2011 | $675 | 12.50 per cent |

| 2012 | $722 | 6.96 per cent |

| 2013 | $800 | 10.80 per cent |

| 2014 | $778 | -2.75 per cent |

| 2015 | $728 | -6.43 per cent |

| 2016 | $709 | -2.61 per cent |

| 2017 | $710 | 0.14 per cent |

| 2018 | $812 | 14.37 per cent |

| 2019 | $847 | 4.31 per cent |

| 2020 | $860 | 1.53 per cent |

| 2021 | $941 | 9.42 per cent |

| Annualised | – | 3.80 per cent |

Table 2

Let’s now run through the different options!

Estimated valuation: $1,300,000

Outstanding loan: $600,000

Manner of holding: 99:1

For buying party with 99 per cent shares

| Description | Amount |

| Valuation | $1,287,000 |

| Outstanding loan | $594,000 |

| New loan | $603,750 |

| 5 per cent option fee (a) | $650 |

| 20 per cent exercise fee (b) | $2,600 |

| BSD (c) | $130 |

| Legal fees (d) | $6.000 |

| Total costs incurred (a+b+c+d) | $9380 |

As both of you are eligible for a maximum loan of $1.2 million individually and with the new loan being half of that, you will be able to decouple the property.

Based on the estimated valuation you provided, we assume you own a three-bedroom unit. Since there was only one rental transaction in Treasure Crest over the last three months at $4,700 for a three-bedroom unit, we have also considered the average three-bedroom rentals in neighbouring projects: Bellewaters at $4,200 (also just one transaction) and The Vales at $4,217. This results in an average rental of $4,372 for all three projects. For simple calculation purposes, we will round this figure up to $4,400.

We will do a five-year projection based on:

| Time period | Total costs | Total gains | Profit |

| Starting point | $4,882 | $0 | -$4,882 |

| Year 1 | $43,219 | $102,200 | $58,981 |

| Year 2 | $85,623 | $206,277 | $120,654 |

| Year 3 | $122,559 | $312,303 | $189,744 |

| Year 4 | $163,500 | $420,351 | $256,851 |

| Year 5 | $198,910 | $530,499 | $331,588 |

Table 3

In five years, you could potentially make a profit of $331,588 from Treasure Crest.

Now, let’s say you were to purchase another unit at $1.8 million for your own stay.

| Description | Amount |

| Assuming the maximum eligible loan | $1,200,000 |

| BSD | $59,600 |

The annualised growth rate of resale non-landed private properties (excluding ECs):

| Year | Avg PSF of resale non-landed private properties | YoY |

| 2000 | $667 | |

| 2001 | $561 | -15.89 per cent |

| 2002 | $536 | -4.46 per cent |

| 2003 | $495 | -7.65 per cent |

| 2004 | $496 | 0.20 per cent |

| 2005 | $527 | 6.25 per cent |

| 2006 | $645 | 22.39 per cent |

| 2007 | $812 | 25.89 per cent |

| 2008 | $750 | -7.64 per cent |

| 2009 | $777 | 3.60 per cent |

| 2010 | $954 | 22.78 per cent |

| 2011 | $1,083 | 13.52 per cent |

| 2012 | $1,169 | 7.94 per cent |

| 2013 | $1,287 | 10.09 per cent |

| 2014 | $1,216 | -5.52 per cent |

| 2015 | $1,219 | 0.25 per cent |

| 2016 | $1,273 | 4.43 per cent |

| 2017 | $1,312 | 3.06 per cent |

| 2018 | $1,356 | 3.35 per cent |

| 2019 | $1,395 | 2.88 per cent |

| 2020 | $1,353 | -3.01 per cent |

| 2021 | $1,402 | 3.62 per cent |

| Annualised | 3.60 per cent |

Table 4

Similarly, we will do a five-year projection for this own-stay property based on:

| Period | Total Cost | Total Gains | Profit |

| Starting Period | $59,600 | $0 | -$59,600 |

| Year 1 | $117,672 | $64,800 | -$52,872 |

| Year 2 | $174,381 | $131,933 | -$42,448 |

| Year 3 | $229,667 | $201,482 | -$28,185 |

| Year 4 | $283,469 | $273,536 | -$9,933 |

| Year 5 | $335,723 | $348,183 | $12,460 |

Table 5

At the end of five years, you could potentially make a profit of $12,460.

Total profits from Option 1: $331,588 + $12,460 – $9250 (cost of decoupling minus BSD of $130 since it’s already included in the total costs) = $334,798

As you mentioned, in this situation, additional legal fees will be associated with the decoupling process compared to selling Treasure Crest immediately. However, it will grant you more time to find a suitable property, which is a valid concern given the current market conditions. But how will this impact your potential profits?

Costs of decoupling: $9,380

For your own stay property, we will refer to Table 5 in Option 1.

Let's say you were to take a year to find a suitable investment property, but in the meantime, you're still renting out Treasure Crest at $4,400/month.

The following is a projection for holding onto Treasure Crest for a year based on:

| Time period | Total costs | Total gains | Profit |

| Starting point | $4,882 | $0 | -$4,882 |

| Year 1 | $43,219 | $102,200 | $58,981 |

Potential profits from decoupling and holding onto Treasure Crest for a year: $58,981 – $9,250 (cost of decoupling minus BSD of $130 since it’s already included in the total costs) = $49,731

Selling Treasure Crest

| Description | Amount |

| Price of Treasure Crest in a year’s time based on a 3.8 per cent growth | $1,349,400 |

| Outstanding loan after a year | $587,923 |

| Estimated cash and CPF proceeds from the sale | $761,477 |

[[nid:623867]]

By selling Treasure Crest, you would unlock approximately $760,000 in funds, which could either augment your budget for the investment property or be set aside as emergency funds or allocated to other forms of investment.

Assuming you were to set aside $360,000 and invest the remaining $400,000 in your investment property, this would bring your budget to $2 million to $2.2 million, depending on the buyer.

Since you plan to make this purchase a year later, we will conduct a four-year projection instead, so that we compare the same time period as with Option 1.

The following is a four-year projection based on:

| Period | Total Cost | Total Gains | Profit |

| Starting Year | $75,000 | $0 | -$75,000 |

| Year 1 | $140,949 | $132,000 | -$8,949 |

| Year 2 | $210,836 | $266,592 | $55,756 |

| Year 3 | $273,800 | $403,869 | $130,069 |

| Year 4 | $340,574 | $543,929 | $203,354 |

Table 6

At the end of four years, you’ll potentially make a profit of $203,354 from your investment property.

Total profits from Option 2: $49,731 + $12,460 + $203,354 – $9,380 = $256,165 (This is not including the $360,000 set aside from the sale of Treasure Crest)

In this scenario, the optimal outcome would be to find a suitable property for your own stay or investment that aligns with your selling timeline, allowing you to have a place to stay after the sale. Alternatively, you could temporarily move into a friend or family member's home if possible.

However, if neither of those options is feasible, the worst-case scenario would be having to rent until you can find a suitable place. Given the current demand for rental properties, landlords may prefer tenants with longer leases, meaning you may have to commit to renting for at least a year.

Let's take a look at how this will pan out in the various scenarios.

Selling Treasure Crest now

| Description | Amount |

| Selling price | $1,300,000 |

| Outstanding loan | $600,000 |

| Estimated cash and CPF proceeds from the sale | $700,000 |

As before, we will put $400,000 towards the purchase of the next property and set aside $300,000.

Buying own-stay property at $2 million (timeline aligns with sale).

The following projection is based on:

| Period | Total Cost | Total Gains | Profit |

| Starting Year | $69,600 | $0 | -$69,600 |

| Year 1 | $128,472 | $72,000 | -$56,472 |

| Year 2 | $185,981 | $146,592 | -$39,389 |

| Year 3 | $242,067 | $223,869 | -$18,198 |

| Year 4 | $296,669 | $303,929 | $7,259 |

| Year 5 | $349,723 | $386,870 | $37,147 |

Table 7

Buying the investment property a year later at $1.8 million

The following is a four-year projection based on:

| Period | Total Cost | Total Gains | Profit |

| Starting Year | $59,600 | $0 | -$59,600 |

| Year 1 | $117,629 | $64,800 | -$52,829 |

| Year 2 | $174,196 | $131,933 | -$42,264 |

| Year 3 | $229,240 | $201,482 | -$27,758 |

| Year 4 | $282,694 | $273,536 | -$9,158 |

| Year 5 | $334,489 | $348,183 | $13,694 |

Table 8

Total profits, if you can find a suitable property for your own use that aligns with the timeline of your sale and the purchase of the investment property a year later (or vice versa), would be: $37,147 + $13,694 = $50,841. This figure does not include the remaining $300,000 proceeds from the sale of Treasure Crest.

Now, let’s examine the worst-case scenario.

The average rental price per square foot (PSF) for private properties over the last two months of 2023 is $4.78. Assuming you rent a two-bedroom unit at 800 square feet, that would amount to $3,824 per month. If you were to rent for a year, the cost would be $45,888.

Let’s say you were to buy both your own stay and investment properties the following year.

Buying own stay property at $2 million one year later

The following projection is based on:

| Period | Total Cost | Total Gains | Profit |

| Starting Year | $69,600 | $0 | -$69,600 |

| Year 1 | $128,429 | $72,000 | -$56,429 |

| Year 2 | $185,796 | $146,592 | -$39,204 |

| Year 3 | $241,640 | $223,869 | -$17,771 |

| Year 4 | $295,894 | $303,929 | $8,034 |

Table 9

For the investment property, we can refer to Table 8.

[[nid:623631]]

Total loss if you were to rent and purchase both properties one year later: $8,034 + $13,694 – $45,888 = -$24,160 (this is not including the remaining $300,000 proceeds from the sale of Treasure Crest)

You can see that in this case, the appreciation in the properties and income from your rental property can't outweigh the cost of rental plus the interest cost of the loan.

Let's also contemplate a situation where you are lucky enough to acquire both properties within the same year that you sell Treasure Crest, without the need to rent any interim accommodations.

The following projection is based on:

| Period | Total Cost | Total Gains | Profit |

| Starting Year | $64,460 | $0 | -$64,460 |

| Year 1 | $128,772 | $118,800 | -$9,972 |

| Year 2 | $196,581 | $239,933 | $43,352 |

| Year 3 | $258,107 | $363,482 | $105,375 |

| Year 4 | $323,009 | $489,536 | $166,527 |

| Year 5 | $381,503 | $618,183 | $236,680 |

Table 10

Refer to Table 7 for own-stay property.

Total profits if you’re able to buy both properties in the same year you sell Treasure Crest without having to rent: $37,147 + $236,680 = $273,827 (this is not including the remaining $300,000 proceeds from the sale of Treasure Crest)

It is important to note that our calculations are basic, and these figures may vary depending on market conditions.

Since your primary objective is to achieve rental returns and capital gains, we will examine the potential gains or losses to determine which option will yield the best returns.

| Item | Amount |

| Cost of decoupling | $9,380 ($9,250 after deducting BSD of $130 since it’s already included in the costs of holding Treasure Crest) |

| Potential profits from holding onto Treasure Crest and renting it out for 5 years | $331,588 |

| Potential profits from own stay property in 5 years | $12,460 |

| Total profits | $334,798 |

| Item | Amount |

| Cost of decoupling | $9,380 ($9,250 after deducting BSD of $130 since it’s already included in the costs of holding Treasure Crest) |

| Potential profits from renting out Treasure Crest for a year and then selling | $49,731 |

| Potential profits from own stay property in 5 years | $12,460 |

| Potential profits from the investment property after 4 years | $203,354 |

| Total profits | $256,165 |

Scenario 1 – Able to find an investment/own stay property that matches the selling timeline so no renting is required, and buying the next property a year later

| Item | Amount |

| Potential profits from own stay unit after 5 years | $37,147 |

| Potential profits from investment unit after 4 years | $13,694 |

| Total profits | $50,841 |

Scenario 2 – Unable to find a suitable property that matches the selling timeline, will have to rent and purchase both properties one year later

| Item | Amount |

| Cost of renting for a year | $45,888 |

| Potential profits from own stay unit after 4 years | $8,034 |

| Potential profits from investment unit after 4 years | $13,694 |

| Total profits | -$24,160 (not including the remaining $300K proceeds from the sale of Treasure Crest) |

Scenario 3 – Able to buy both properties in the same year you sell Treasure Crest without having to rent

| Item | Amount |

| Potential profits from own stay property after 5 years | $37,147 |

| Potential profits from an investment property after 5 years | $236,680 |

| Total profits | $273,827 (this is not including the remaining $300K proceeds from the sale of Treasure Crest) |

With Options 2 and 3, you would be selling Treasure Crest, unlocking at least $700,000 in funds (including CPF, which must be refunded into your accounts). These represent actual profits, whereas our projections are potential paper gains.

Among the potential profits, Scenario 1 would yield the highest returns as the loan amount for Treasure Crest is considerably lower than what you would need to borrow for a $1.8 million to $2 million investment property, which, given the current high-interest rates, would result in significant interest expenses.

Given the current high-interest rate and limited supply in the market, Options 2 and 3 might not be the most favourable choice, as it involves taking on two significant loans.

Moreover, for Scenario 3 to occur, you would need a stroke of luck to find two properties that meet your needs in such a short period, considering today's low supply.

[[nid:623399]]

Additionally, if you don't have backup accommodation after selling your current property and fail to find a suitable unit within your timeframe, renting could become a substantial expense.

In scenario 1, you benefit immediately given you can rent out Treasure Crest right away.

It must be said that this is also the case because the historical annualised returns for ECs are at 3.8 per cent based on our calculations versus the lower 3.6 per cent for non-ECs.

Another factor you should consider is that options 2 and 3 involve more steps which translate to more effort on your part. Plus, you'll entail extra legal fees, stamp duties and agent fees.

After considering all factors, we think that Option 1 appears to be the most logical decision. By choosing this option, you can promptly rent out Treasure Crest once you relocate to your own property, without the hassle of searching for another investment property.

With Option 1, since you're only selling Treasure Crest in three-five years, you would unlock the $700,000 at a later time. It is also a good opportunity to wait and see if interest rates would fall any lower while relying on rental income for cash flow reasons.

ALSO READ: 5 property asset progression risks upgraders should know to avoid financial setbacks

This article was first published in Stackedhomes.